A little knowledge is a dangerous thing

A little knowledge is a dangerous thing

Most "experts" sit in that ignorant sweet spot

Between ignorance and enlightenment

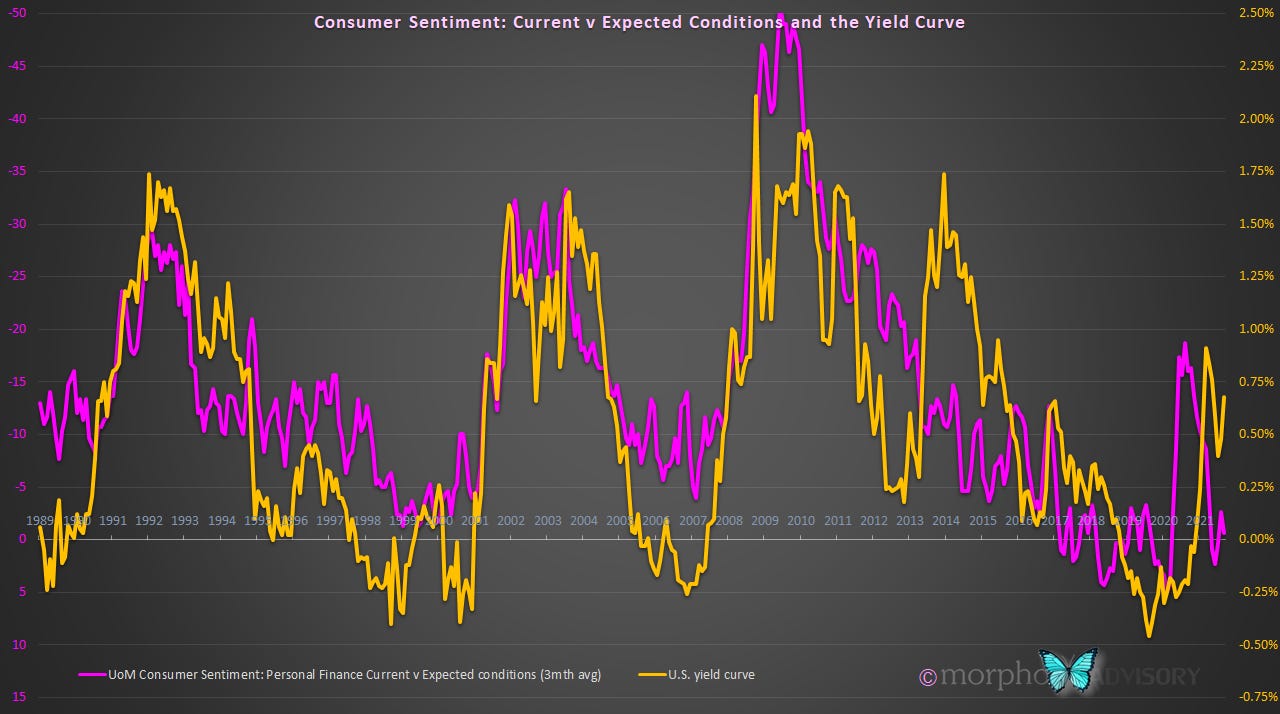

Those of you who have followed my writing or tweeting for any length of time know that I like both the yield curve and consumer sentiment as key sources of useful information.

I like the yield curve because, for the most part, it is the domain of some of the smartest and forward looking people in finance - bond traders.

I like consumer sentiment data because it is the sum of economic behavior by the masses - blind to macroeconomic analysis (other than their own private financial affairs), they just do what they do. It is the collective economic unconscious.

Between these two extremes we have the realm of financial “experts”, which includes asset allocators, investment committees, economists and even central bankers like those at the U.S. Federal Reserve. Schooled in academic understanding, these people can talk the talk and know the theory. They have papers to prove it and, very often, those who sit atop the most influential financial institutions have papers from ‘brand name’ schools and organizations, which simply must guarantee their “expertise”.

I guess what I’m getting at it is, there are two extremes - ignorance, other than one’s own financial affairs, and those who have academic understanding but also possess real-world ‘street smarts’. Between those two extremes is where the market whipsaws people. These middle-ground people are the ones who are driven by prevailing narratives. They only take positions once they are sure that the narrative is robust … which usually means that a trend has been observed long enough to know it is a trend, only for them to enter or exit their position just as the trend ends (e.g. like a Fed tightening cycle causing a recession and market crash). The problem is, there is no accountability for their negative value-add because their ultimate clients are ignorant of the cost imposed upon them, and rating agencies, asset consultants et al. are populated with these same middle-ground people, so the justifying arguments seem cogent to them within the context of the prevailing narrative.

Thanks for sticking with me. I feel better after that rant. I don’t know where that came from. It certainly wasn’t the intent of this article. What was?

The yield curve and the consumer

Ah yes, back to my faithful guides.

My attention was drawn to a direct correlation between the yield curve and consumer sentiment that I hadn’t previously observed. In this particular case, there was a notable disparity that caught my eye. Obviously, a divergence will catch one’s eye, but in this instance, consumer sentiment was also suggesting something that I have been saying for several months. Namely, consumer sentiment is saying that the yield curve should be heading toward another inversion.

Why would this historically strong relationship break down now?

It’s all part of the current economic dysfunction and the concentration of money flows into relatively small part of the economy - i.e. goods, and larger capital goods at that. That’s where inflation is being concentrated. Like a single exit door in a burning building, pent-up consumer demand from lockdown plus diverted frustrated travel funds plus a higher than normal retiring population preparing for their golden years all heading for the same capital goods at the same time.

This has resulted in inflation that has caught the attention of all and sundry and become the prevailing narrative. The common knowledge is that interest rates have to rise to combat inflation. As such, individuals and businesses are fixing the interest rate on their loans, pushing rates up. Asset managers and asset allocators have been pushing rates up by selling their bonds to avoid losses based on the belief that rates will continue to rise. And, last of all, will come the Fed who plan to taper their bond purchasing and have taken pains to get everyone psyched for the event.

Facilitating all of this are the fixed income traders who, like soft style martial artists, dance with the market flows - close enough to feel the strength of their flow-based energy, rather than applying hard style combat approach (i.e. standing their ground and going toe to toe against the market). These traders will back up under strong interest rate selling flows and let the market push rates higher, despite their own belief that interest rates should be moving lower. As the market selling pressure abates, these traders will test the market by buying interest rates (i.e. pushing interest rates lower) to see if the market takes the opportunity to sell more. If they don’t, traders will push rates lower again. If they get lucky, they may cause those who sold (and now realize their folly) to have to stop-out of their position, i.e. chase the market and buy back their losing position.

This is what is happening at present. We are at peak inflation narrative (everyone knows that everyone knows that inflation means interest rates have to rise), yet longer-dated interest rates have begun to fall again, even as short-end interest rates rise. The yield curve wants to flatten … maybe even invert?

It may only take an economic surprise or two to the downside to accelerate this break lower. Let’s wait and see what the data says, shall we?1

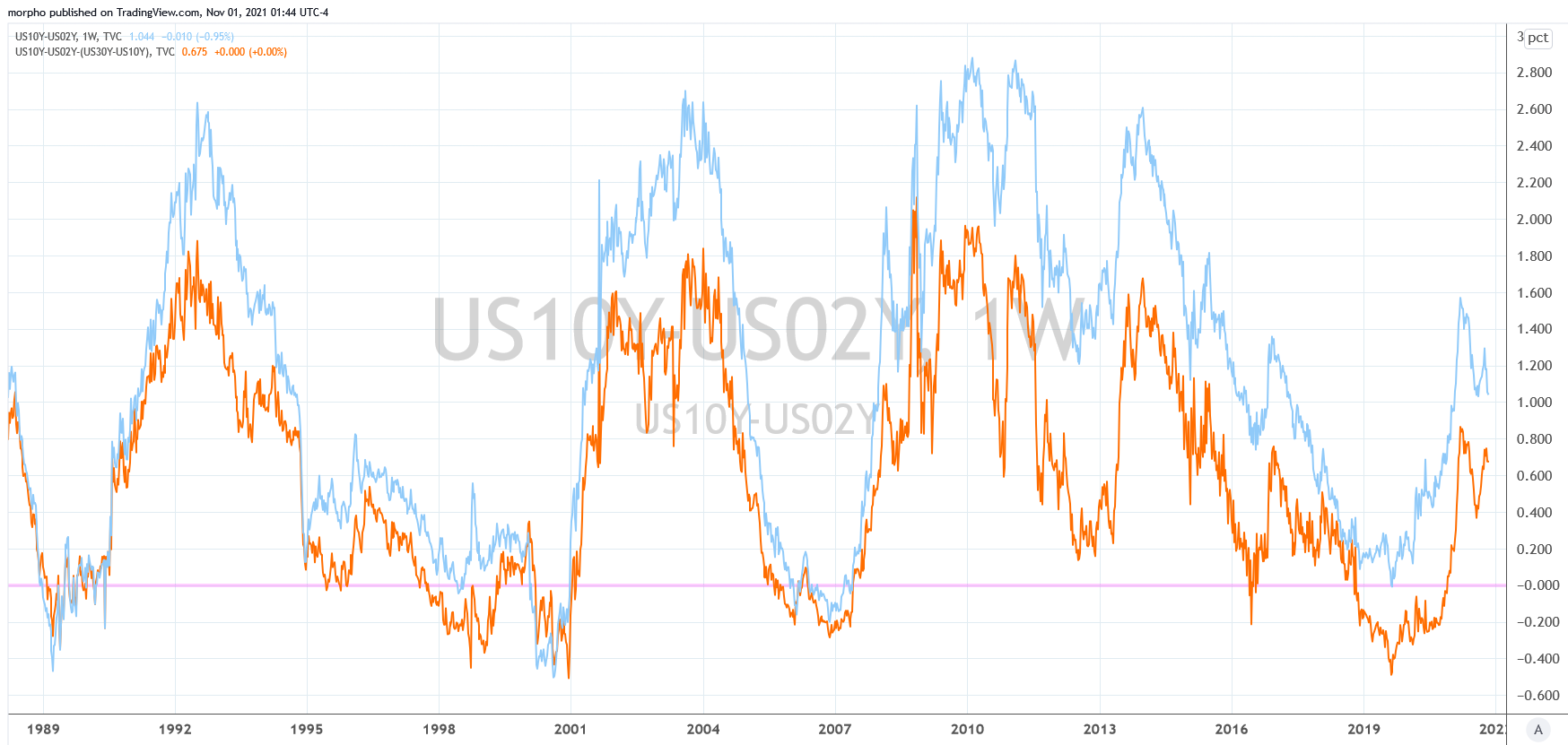

A couple of other charts, just for fun

U.S. 10 Year Treasury Yield

U.S. Yield Curve, two models - the old and the new. Either way, it’s struggling to make new highs

Disclosure: I am invested in bonds at present, so I am talking my book.