Counterintelligence

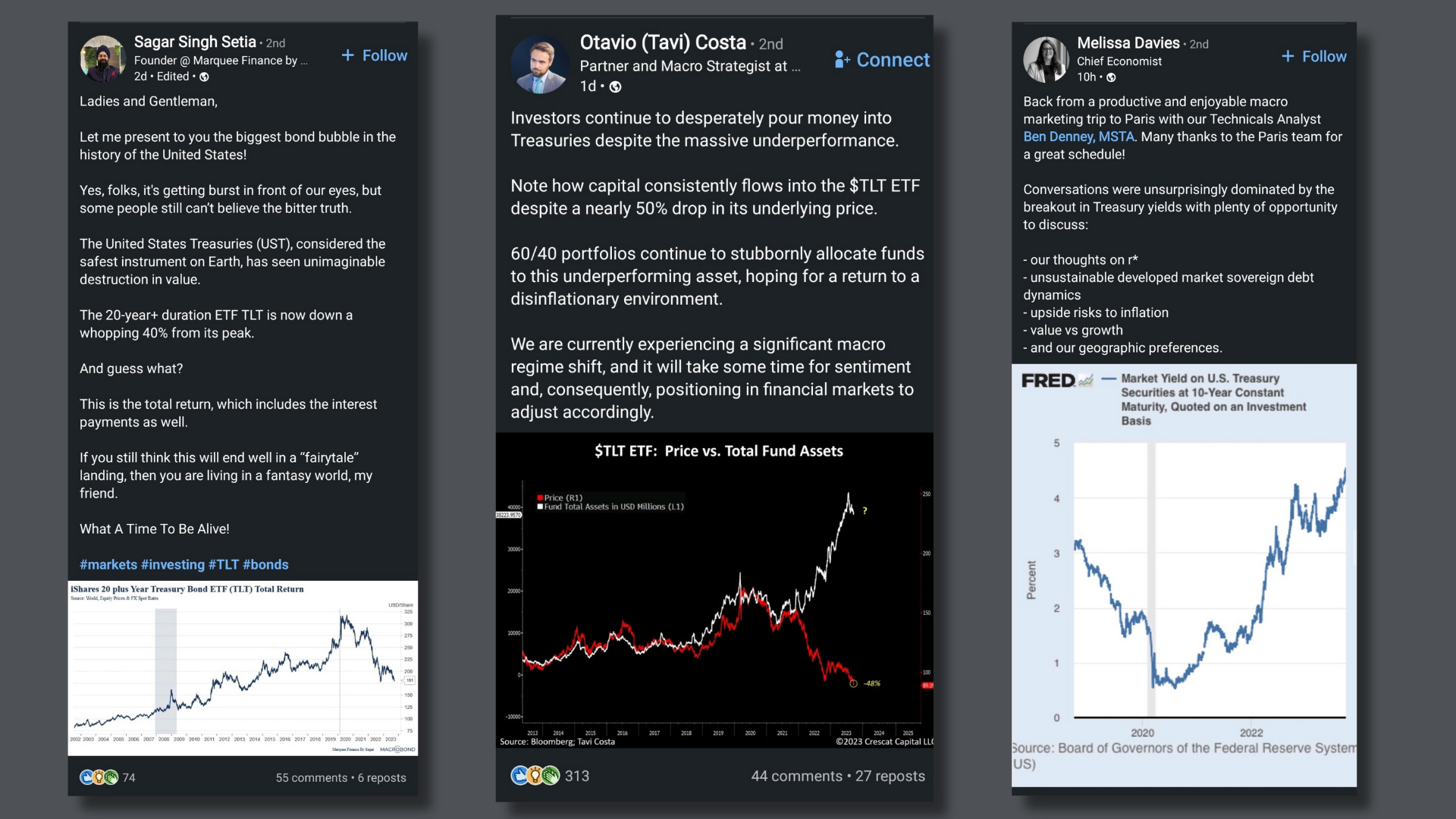

I didn’t realize when I published my last article that I was facing off against the horde. My fault. I hadn’t looked at what topic the social media like-hunters were applying their all-reaching expertise to and upon which they could opine. It turns out that bonds are their flavor of the month … and not in a good way (i.e. “bonds bad”).

I shit you not. The following three posts appeared one after the other when I opened LinkedIn this last week, and I have seen several more along the same lines since.

Social media is a barometer of sentiment, which is a function of price and so we get narrative constructed to fit. In the realm of financial markets, the cart remains ever before the horse.

Can one combobulate the discombobulated? Apparently not, and that’s not just etymologically speaking. There remains a shitload of ‘risk-free’ return on the table while larger risks are evolving elsewhere, but because those risks are not being reflected in the price action, sentiment has not turned its attention in that direction and so narrative is absent.

In the realm of the uninformed, conflating narrative that “explains” current price action with insight is standard practice.

To everything there is a season …

Is it any wonder that the random walk theory and efficient market hypothesis have teamed up to create the widely held belief that there is no knowing? Financial market “experts” essentially tell us the market, like God, is ineffable … but then immediately attempt to describe it anyway.

When you observe the world through a microscope focused on price you lose your peripheral vision and miss the seasonality driven by planetary movement.

… a time to hate bonds

Fixed income took a pasting these last two years because of inflation and the subsequent monetary policy response. For investors, this was especially bad news because stocks took a hit also.

The general belief in the asset management industry is that bonds provide diversification for stocks and so, the majority of investment portfolios the world over are constructed with a mixture of these two asset classes. However, I have observed before that the correlation (or lack thereof) between stocks and bonds is cyclical.

Over the last 100 years or so, the correlation cycle between stocks and bonds has swung from being negatively correlated (good from a diversification perspective) to positively correlated (bad from a diversification perspective) approximately every 20 years.

This means that, generally speaking, we shouldn’t rely on bonds for diversification in our investment portfolio over the longer-term (i.e. the next couple of decades).

… and a time to gather bonds together

Nevertheless, as I explained in my last post, in the shorter-term, there is good reason not to do away with bonds too quickly, and especially not at this point in time. There is shorter-term seasonality within the larger correlation cycle. After central bank interest rate hikes is prime time for bonds.

From Risk-free return to Return-free risk

I posted the following chart in my last article, but I noticed another aspect, which bears consideration.