Fundamentals v Technicals

Fundamentals v Technicals

The new global supply shortage is the most critical yet

Fundamentals v Technicals

For the 30+ years that I have been in markets there has been an ongoing debate about which is better (or more reliable), fundamentals or technicals?

Those who rely solely on technicals typically don’t have the rational explanation for why techincals work, and so they suffer jibes about mysticism and it all being a bunch of nonsense. It is not uncommon for advocates of technicals to use as their summary statement that all available information is reflected in the price. This is somewhat true, although that argument does sound suspiciously like the Efficient Market Hypothesis, which is utter garbage – except in a classroom. In reality, when it comes to technicals, the price does not so much reflect all available information. Rather, the price IS the information, and it is telling us about the collective behavior of the market participants.

The linear thinking world of those who only trust fundamentals demands rational explanation for market price moves. The rational minded world is the domain of big financial institutions, government financial agencies, mainstream media (MSM) etc. Rational explanation aligns with their need to project intelligence, especially in their published and public content. The citizens of this world confuse correlation with causation. Or, more accurately, they confuse catalysts with causation when it comes to explaining market moves.

The reason technicals work is that the setup for market moves is hidden in plain sight - in the price information. The rational minded confuse an event - the catalyst for a dramatic move - with the cause. The cause of price movement is the market being asymmetrically exposed position-wise. MSM & other market mavens will cite the catalyst ad nauseam as being the driver behind market moves. In reality, the market got itself too short or too long and a triggering event (the catalyst) resulted in position covering, which is what makes the move look dramatic (or surprising, e.g. like yields falling when inflation is rising) – because people are losing money and are in a hurry to make it stop.

Let’s look at a recent example

Those who ascribe to the fundamentals worldview sarcastically say things like, “Oh sure, technical analysis foresaw that central banks would suddenly change their mind about being slow to move against inflation.” But what technicals do via observing price action is not see a specific catalyst, but rather that the market is positioned for an asymmetric outcome, e.g. positioned for a continued steepening in the yield curve. Because this positioning was widespread (and also highly leveraged, which makes it the weakest market position – i.e. unable to endure financial pain), it was getting increasingly harder for the yield curve to steepen, because everyone was already positioned that way and they needed new market participants to jump onto this same position for long rates to continue to push higher, of which there weren’t many left. As such, it was relatively easy for bond markets to move longer-dated interest rates (bond yields) lower, which resulted in several hedge funds experiencing billions of dollars in losses (e.g. Rokos, Alphadyne etc.). All it took was a normally relatively benign act of some central banks doing a little thinking out loud. The market was just looking for an excuse to move.

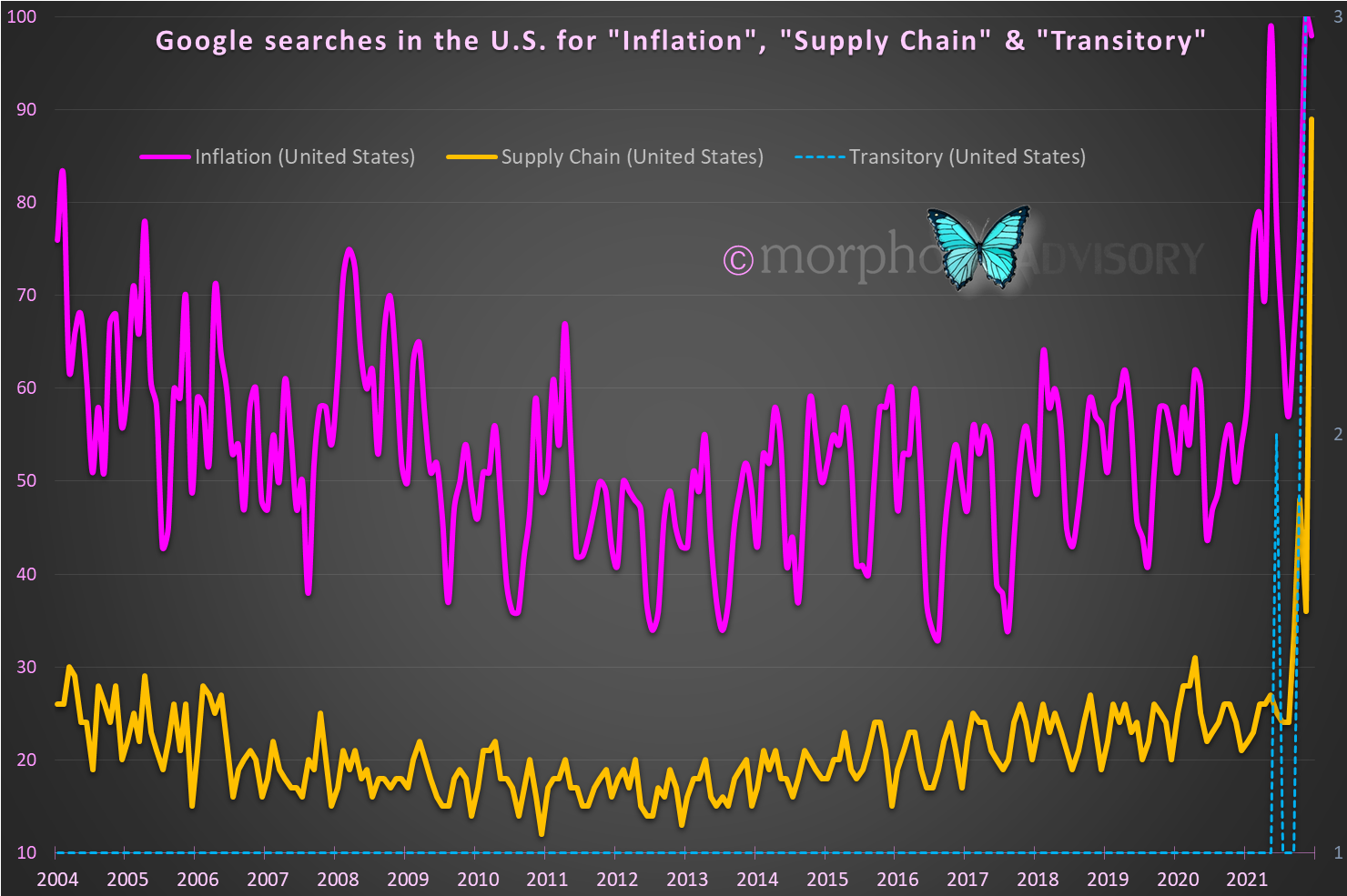

Inflation, transitory and supply chains

So, what’s the current setup? At present, under cover of the noise from the prevailing narrative around inflation, there is anecdotal evidence that companies are raising their prices to increase profit margins and blaming it on inflation and supply chain disruption (i.e. getting away with selling at higher prices because they think they can – consumers are expecting it). This is why I believe that inflation is remaining high while the underlying economic activity is lacking vitality, as demonstrated by weak consumer sentiment, falling global shipping costs and flat global trade and production data. This error of judgment by businesses (i.e. short-term thinking) is deceiving the Fed into the need to act precipitously at what will prove to be precisely the wrong moment for the long-term wellbeing of the economy … that is to say, this will be how the Everything Bubble will die. However, let’s not be too harsh on them.

Central bank policy committees, like all holders of senior positions in public office, are essentially politicians – that’s how they got their position. Because of this, they are very sensitive to public opinion. When the heat comes on them they are swayed by the pressure to appear as having everything under control, but little by little they feel forced to follow sentiment and prevailing narrative. They make speeches (like all politicians) about only acting having given due consideration, which is a politician’s ploy to buy time to move toward pleasing the crowd while also maintaining the perception that they know what they’re doing. They possess no special insight and have no greater talent than any other of the ‘fundamentals only’ persuasion, despite the resources at their disposal. They are out of their intellectual depth but they don’t know it.

So, it’s technicals by a knock-out then? Not so fast …

Thus far I have made it sound like I am firmly in the technicals camp and anti-fundamentals. That is not true at all. I believe in an integrated practice where both should be part of the process in forming a cohesive and robust view of the economic landscape. All technicians would benefit from an understanding of fundamentals as a check against their analysis. I look at data from both perspectives and let that data tell me what is going on, i.e. both the fundamentals and technicals must be in agreement. If they are not in agreement then my interpretation needs reevaluation.

This year it has proven a successful approach. While the financial world has gone crazy over inflation; mocked the word “transitory”; and suggested longer-dated yields will continue to rise, I have held the view that the yield curve is going to flatten – and probably invert again. I even moved my retirement portfolio into longer duration bonds in mid-October, contrary to the prevailing narrative. I’m hoping to capture the bond market’s last hurrah and tell my grandkids that I was there when the bond market finally died.

Integrating both fundamentals and technicals is the essence of a market strategist, but there are many with that label who still struggle and can’t create a holistic picture of the state of play.

The fundamentals camp is essentially the domain of economists – linear thinkers who rarely get anything of significance right but can talk a good story.

The technicals camp is the domain of technicians – pick whatever method you like, get familiar with it, then by applying good risk controls and discipline you can make it profitable despite not having any idea about what is going on.

Strategists – integrate both fundamentals and technical-based disciplines in a holistic manner, but despite being in a better position than either the fundamentals or technicals camp it only goes to highlight the weak link of either fundamentals or technicals …

Interpreters - the real supply shortage

I’ve said it before on this site. It is something I have observed across multiple disciplines, not just financial – it is a human thing. The ability to interpret information (i.e. with a skill that surpasses a simple linear explanation, but with real insight and understanding) is an extremely rare skill. And when I say rare, I mean a mere handful on a global basis (at least with talent at a level, quality and consistency that merits attracting a degree of attention or fame) in any single discipline. So then, very rare.

Just because someone is a strategist, it is still not reason enough to believe they have got the right outlook on markets and the economy. We all get some things right from time to time. By all means, find people whose work you like, absorb information from them and develop your understanding, but do your own thinking and don’t become affiliated in your own mind that you blindly adopt another’s opinion out of a sense of allegiance. Perhaps you will become one of those rare people who will develop into the mere handful that can successfully interpret the financial world and be of use to nations or the global population. God knows we need some talent in that area now for the decades that lie ahead as a result of the mismanagement of decades past.