Going soft on the economy

Assuming it can't be tested, so it's all down to interpretation

Soft science

Social sciences (or soft sciences) like economics operate under the umbrella of inductive reasoning where generalizations are made based on observation (i.e. interpretation), but it is believed that these observations can’t be tested, so no effort is applied in that direction. This method is so entrenched that people operating in these spheres never think to apply other methods, e.g. deductive reasoning. Fortunately for me, I didn’t know any better so went ahead and did it anyway. I applied the inductive approach and, importantly, applied a different interpretation to my observations than the ‘educated’ economic consensus, and then tested the hypothesis with hard data. The data agreed with my interpretation of the economy and proved to me that thems what’s in charge of overseeing our financial systems don’t really understand what they’re doing. They are highly trained people, but highly trained to think in an incorrect manner and interpret information in the wrong way. I don’t know, maybe it’s autism or maybe it’s because I did a course in exegesis? Whatever. What is clear is that soft sciences like economics would do well to challenge their assumptions and test (or re-think) their interpretations rather than assuming it can’t be done.

Institutional media Denial-of-Service attack

In my last post, I pointed out the fact that in every cycle we get people denying recession will occur or that there will be a “soft landing”, which means that if there is a recession it won’t be so bad. This usually happens when a recession is already underway (the examples I showed in my last post were all made when the economy was already in recession, but it just hadn’t been officially declared until some months later when NBER said that recession began a year earlier). This goes to show that recession is not obvious when you are in it. Recession only becomes obvious toward the end when large numbers of people begin losing their jobs. As I have noted before that our financial experts miss, rising unemployment doesn’t cause a recession (although it is coincident when a recession is finally declared), a recession causes rising unemployment (falling spending means cost-cutting, which results in layoffs). You have to go back to WWII for the last time that Nonfarm Payrolls weren’t growing at the start of a recession, yet the Fed and others take comfort in the strong labor market as they continue hiking interest rates.

The Fed came out recently and added their voice to the growing number of people conflating the stock market with the economy. “No recession” is now their base case. Unbelievable!

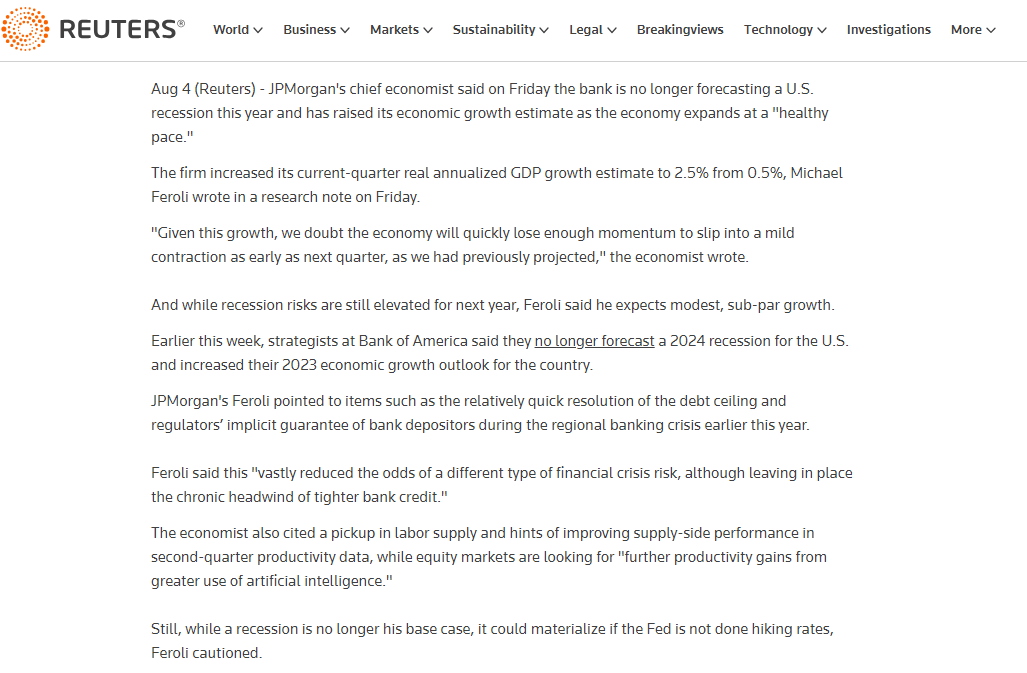

Bank of America and JP Morgan have joined the ranks of institutions who have backed off (or pushed out) their recession calls. They claim it’s because of the strong data (what data?), but I suspect the truth is because of the interpretive nature of their science (what interpretation?), which can be swayed by sentiment (that irrationally exuberant stock market has a lot to answer for) and social pressures (and possibly even internal institutional pressures).

So here we are, almost certainly ankle deep in a recession already, yet every “expert” is saying that it can’t be so.

Perhaps people should try taking a non-expert perspective and take a sample observation from their own life - a process sometimes referred to as “common sense”. What we personally are experiencing (and maybe even see a number of other people we know are also experiencing) is not localized or specific to us. The cost of living has gone up and higher debt-servicing is limiting budgets and constraining behavior (e.g. not selling houses because don’t want to lose low interest rates). People are in cost-cutting mode, looking for places where they can make savings. This is impacting corporate earnings, which have been experiencing downgrades as reflected in deteriorating CEO Confidence, weakening PMIs, negative real retail sales etc.

The Fed’s rapid and massive rate hikes (along with every other developed nation central bank) in a world that is overburdened with debt, with populations having gone all-in during the post-Covid ‘free money’ boom, IS INCOMPATIBLE WITH A SOFT-LANDING OR NO-LANDING ECONOMIC SCENARIO. IT’S HARD-LANDING ALL THE WAY!

The data validates my outlook using an inductive approach to develop a hypothesis and then a hard science approach to validate it.

To make matters worse, the monetary pressure is likely to remain on for some time yet … if it doesn’t get even tighter. I say this because the price of oil has been rising of late, which may put a pause in the rapid descent in the rate of inflation.

If the price of oil stays at current levels or even rises over the next couple of months, then this will indicate the fight against inflation has further to go. The current price of oil is the same as it was in September 2022 and is higher than it has been since December 2022. As such, the process of time will impact year-over-year inflation, changing oil’s impact from being disinflationary to possibly being inflationary again.

How can I assert this? Purely by dividing the year-over-year percentage change in the price of oil by 30 and then adding 2%, we get a proxy for the U.S. inflation rate.

If oil’s year-over-year price stops being disinflationary or becomes inflationary, then the Fed may prolong holding interest rates at current high levels … if they don’t turn the tightening taps some more to achieve their objectives.

I remind my professional colleagues that “It ain't over ‘til the fat lady sings”. The economic cycle is slow moving and has a long finale. Haven’t they read the script?

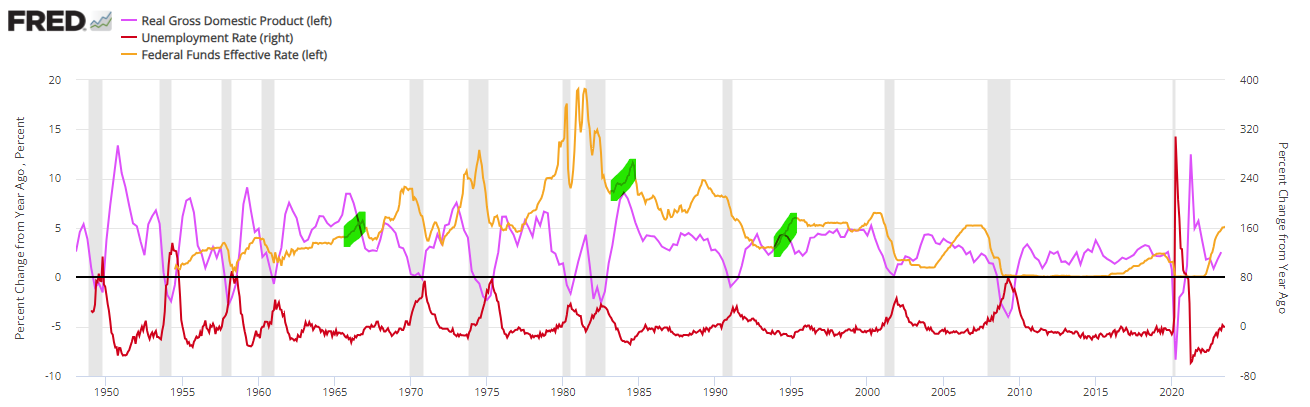

Soft landings are rare - the exception, not the rule. There are three potential occasions that are considered “soft landings”. These are times where the Fed hiked interest rates and a recession did not follow: 1964; 1984; 1995.

I would argue that that the hiking in 1964 was offset by the Baby Boomer generation entering the economy, which expanded the economy even as monetary policy tried to constrain it. Nevertheless, the Fed’s actions did lead to the stock market fall in 1966.

Similarly, the 1995 Fed tightening was offset by that other large population group joining the economy - the Millennials, but the Fed hiking did lead to problems in emerging markets (Asia & Russia) who rely on hard currency (USD) financing which resulted in the demise of LTCM that required emergency policy actions.

The 1984 example is different. This was just after the double dip recessions of the early 1980’s and interest rates being in the vicinity of 20%, so people were still cautious and running prudent levels of financial leverage because the general mindset at the time was that interest rates can, and do, go up. Still, it did result in the 1987 crash.

Are you starting to see the lag between Fed hiking cycles and subsequent stock market impact? It’s very rarely an immediate cause and effect situation. Give it time. They only started hiking in March 2022.

Additionally, there is no population bubble coming to the rescue this time to soften the landing.

Hard science says hard landing.