We’re in that in between space, like the top of the arc in parabolic flight that induces a feeling of weightlessness and is used to train astronauts.

The current environment is also like the view from a cantilevered construction that gives an unobstructed viewpoint inducing a euphoric perspective of being some place special. But what are these feelings (and the underlying economic environment) anchored in?

Back in 1995, here in New Zealand, there was a terrible tragedy in which 14 people died, 13 of whom were students. They all stepped onto a platform that extended over a 40 metre (130 foot) chasm over rocks below. An unquestioned faith in the appearance of a well constructed platform resulted in this terrible event. The failure was in the construction of the cantilevered platform which, among other things, was not securely anchored and so toppled into the chasm forward under the weight of the students.

I don’t use this tragedy as an analogy flippantly. It is against such shoddy construction that I am angered - at society’s blind adoption of an appearances-based approach to problems, be they physical construction or societal constructs. Avoidable tragedies.

First the good news

GDP growth for the third quarter of 2023 was revised up in the U.S. to 5.2% and the Chicago PMI came out at 55.8 (above 50 means growth) - the first expansionary number in a year. Great headline stuff with all the appearance of a robust structure. On top of that, the stock market has remained elevated.

And now the bad news

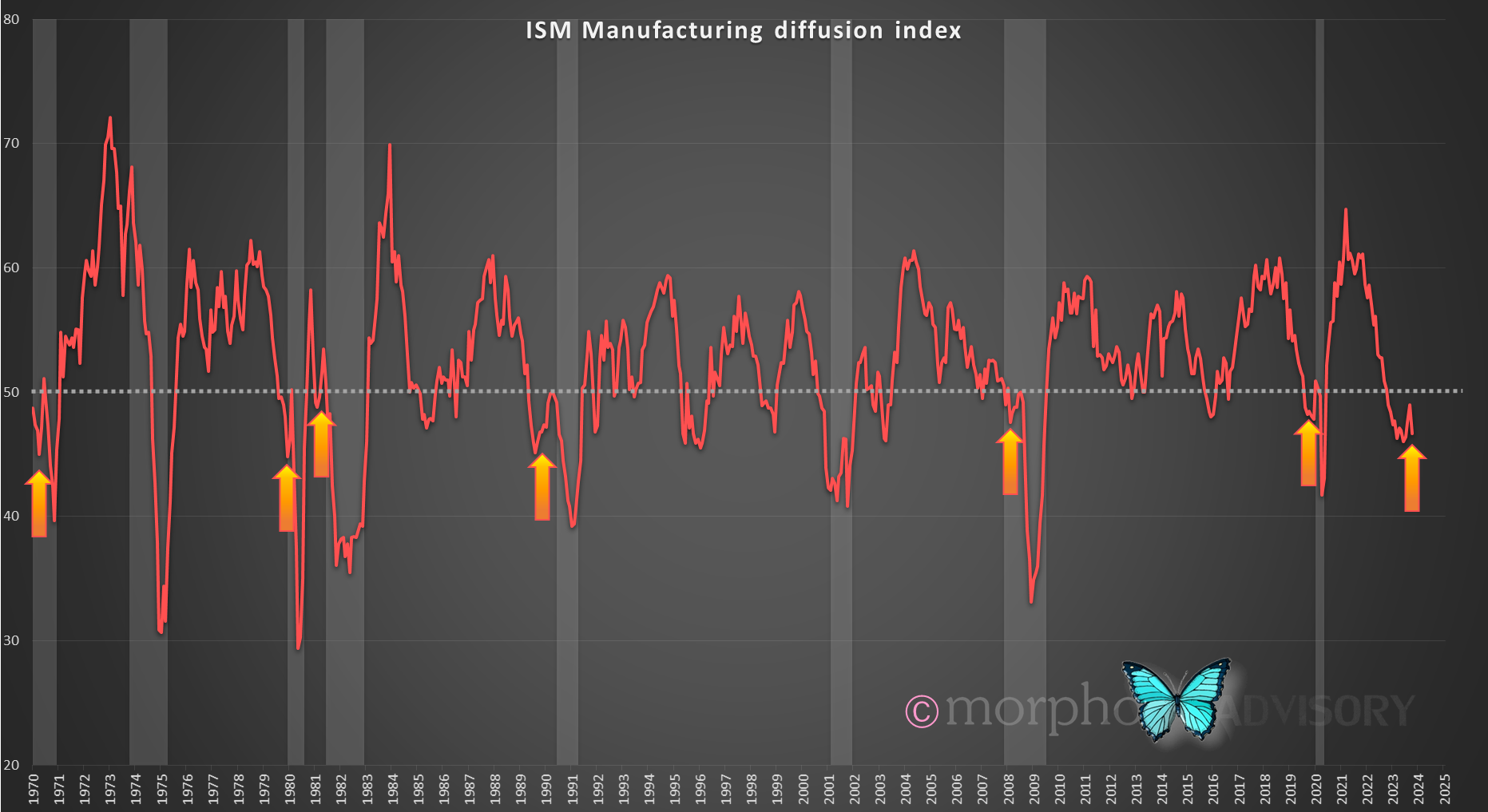

PMI indices and GDP growth are highly correlated, but PMI index releases are more timely than GDP and not subject to revision. My Philly Fed leading indicator suggested that there would be a temporary improvement in economic activity. However, that leading indicator has turned back down (below 50 means contraction). In actual fact, despite the appearance of a rising trend in my Philly Fed leading indicator in the chart below, this indicator only posted a positive number (above 50) for a single period in almost 18 months, and that was 4 months ago.

If we look back over the history of the ISM Manufacturing Index, we see that it has been common for there to be an initial contractionary period followed by a brief recovery before a more severe economic downturn.

In fact, it happens at the onset of the majority of recessions (6 of the last 8). Speaking of recession …

The same ‘double dip’ pattern is observable in the search for the term “recession” on Google:

once when forward looking people warn of a coming downturn; and

then again when it’s actually happening.

In between times is when everyone asks, “Where’s this recession you speak of? I can’t see it.” and officialdom plus Wall St. economists talk “soft landing.” People are so impatient.

What’s behind this ‘First Boston’ two-step?

Here’s what I think is behind this behavioral pattern:

The first dip in economic activity is household cash flow being impacted due to central banks rate hikes because of inflation or the risk of inflation. It reflects change in household’s economic conditions. The second dip is the corporate response to changing economic conditions (i.e. reduced earnings). It’s a form of reflexivity. The household cash flow gets squeezed because of monetary policy, so discretionary spending slows. This impacts businesses who initially try to ride it out and often use accounting tricks to try and smooth their earnings for the next year, but ultimately they have to cut costs. This results in job losses, which causes households to get more defensive in their spending because of the uncertain economic environment (i.e. will I still have a job?).

So, enjoy this brief respite between recessionary bouts.

Book recommendation

I’m sure most of you are not as old as me, so you may have never encountered this book before: “Bombardiers” by Po Bronson (published in 1995). It’s a novel, but still educational in a perverse way, plus a fun read to boot. It’s a farcical take on bond markets from the perspective of an investment banking bond sales desk.

I hadn’t read this book in a while and picked it up again recently. It always makes me giggle because in it’s attempt to send up investment banks and the bonds they try to push on to their investing clients, it is closer to the truth in many respects than most take-themselves-seriously Wall St. types will admit. The fact that the content is still relevant today is scary.

Anyhow, a good read for the holidays.

Unemployment

Yep, still on the watch for unemployment related stuff. Here’s a new chart based upon different data that confirms the same outcome …