Mixed messages

Clarity amongst confusion

The S&P 500 Index has just made a new all-time-high. That’s impressive and certainly not something I would’ve expected a year ago. Nevertheless, I remind you all that the stock market is not the economy and that it is, in fact, the market that serves the economy and not the other way around.

The last time that the market pushed to new highs while the economy was this weak was in 1990, and that turned suddenly.

Of course, what we’re all waiting for is unemployment to rise, which really takes the heat out of sticky inflation because it changes employees attitudes from ‘we need a pay rise to keep up with a rising cost of living’ to ‘I’m not going to ask for anything because I may get laid off’.

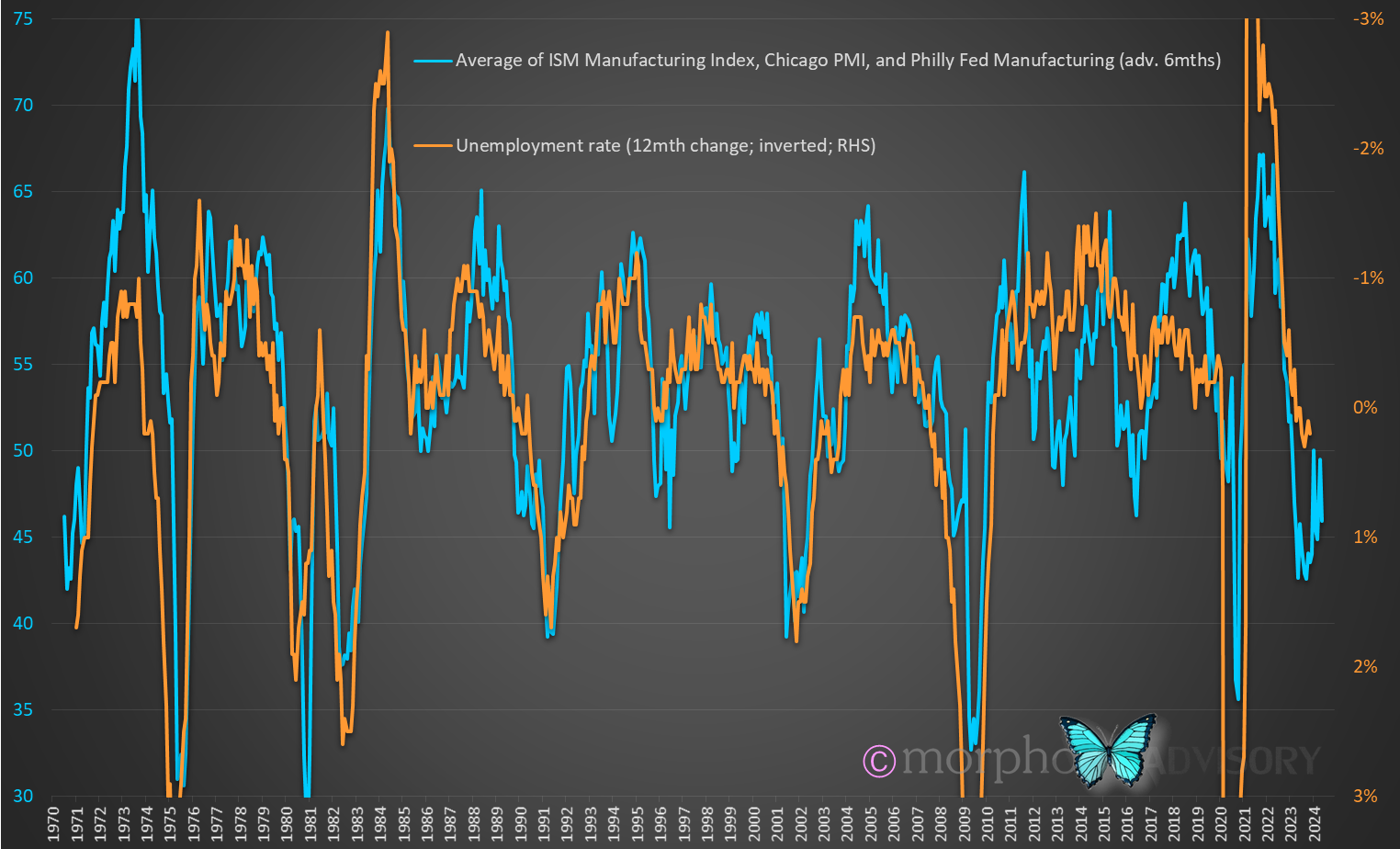

Purchasing Manager Index (“PMI”) data, like in the chart above, is a good proxy for the health of the underlying economy. Looking at PMI data we see a strong correlation with the annual change in the unemployment rate, which makes sense:

if the economy is weak, then people lose jobs; and

if the economy is strong then there are more jobs available.

The following chart shows that, based on the current health of the economy, unemployment should be approximately 1% higher in 6-months time, which implies approximately 2 million Americans will lose their jobs.

When people lose jobs, they stop spending. The reason people get laid off is because people have already stopped spending. This is the reflexive nature of economics at work and that’s why we often see a period of initial weakness, then a slight recovery, which is followed by a second, more substantial period of weakness that everyone recognizes as “being in a recession” even though the real recession started earlier, but just hasn’t been officially declared yet.

So, while market sentiment is buoyant (as per the chart below), rest assured that in boardrooms and executive suites around the world, plans are being made and implemented to reduce operating costs and maintain profitability (i.e. redundancies are coming).

However, sentiment is too easily swayed by price action. It’s fickle, which is why investors are most bullish (green) at the top and most bearish (red) at the bottom.

I did a bit of tinkering with the above chart to convert the survey results to Z-Scores (that’s a measure of how far away from the average current sentiment is when measured in terms of standard deviation).

Investor optimism is nearing the upper end of the historic range, presently (almost 2 standard deviations above the 3-year mean).

Then, of course, I wanted to know how this output lines up with economic data.

The only times when investor sentiment was this positive while economic data was this weak were:

the mid-nineties (I’ve already pointed out before that this period was distorted by the Millennials joining the economy and coming to the rescue); and

2001, when the Dot-Com bust was only halfway through but investor/speculators thought the bottom was in.

Here’s the same chart as above, but with shading to show when investor sentiment was positive while economic conditions were weak.

I present the data to you here so that you can ask yourself whether you’d rather invest because you feel good about things, which is mostly dependent upon the price going your way, or whether you prefer to invest with knowledge that the stock market is standing on ground that has a sinkhole forming beneath it?

The only thing that could save the market is if there was another population bubble waiting in the wings, about to come of age, just like in the mid-nineties. That’s a reflexive economic reality, too. As younger generations get priced out of homeownership, they stop family formation, which then causes the economy to weaken in future decades. This is exactly the scenario that Japan finds itself in.

I tell ya, our economic system is fucked! Economics is about incentives, and the incentives our economic system has created is one of leveraged asset price speculation that places increasingly higher burdens on subsequent generations until they can’t. And that’s where we find ourselves today. Tipping point.

These next couple of decades are gonna be a lesson for people in real world economics. So, while the world’s leaders gather in Davos to hire prostitutes and discuss theoretical economics and policy, I ask you to assess your economic dependencies and exposures. Do a risk assessment of where you are vulnerable and contemplate what might happen to cause you to lose one or more of those things (think ‘far out’ scenarios). What would you do?; how would it impact you? In essence, you’d be asking yourself about loss of income or having high fixed cost structures (e.g. debt). Consider moving countries; having multiple streams of income; living very alternative ways compared to what is traditional etc.

Well, that’s another Cassandra prophecy delivered. I didn’t intend to make it end so doom & gloom, but that’s the facts though you may not realize it or believe it. I genuinely write this shit because I have people’s welfare at heart and want them to be prepared and not be impacted detrimentally.