Money, money everywhere

Transference during a period of reduced options

Headlines and media noise surround us. We get caught up in sound bites and what we see with our own eyes in our local communities. Because of this addiction to noise, few take that needed step back to evaluate what is really going on, and even fewer ask themselves what is missing. There is no investigative journalism in the media nor is there any financial research in the wealth management industry that goes beyond scratching the surface. Thus, we find the majority of supposed and so called financial experts falling for the delusion. “Growth!” “Inflation!” … blah, blah, blah.

Absence of evidence ≠ Evidence of absence

We’re all aware of it in the periphery of our minds, but we haven’t given it much in-depth thought: COVID-19 has had a major impact on the global economy. The world was stopped in an instant, but in our technological age, humanity quickly adapted to life and commerce being conducted online. The travel industry however remains decimated, with the timeframe for its ultimate recovery uncertain. And that’s where this article is headed.

Approximately $4.7tn was spent worldwide on leisure travel in 2019, but only $2.4tn in 2020. The U.S. accounted for $1.9tn in 2019 and only $1.1tn in 2020.

When travel is combined with tourism, it made up approximately 10.4% of global GDP at $9.2tn in 2019. Those numbers were 5.5% and $4.7tn in 2020, respectively. Tourism & travel was a growing component of the global economy. The question I ask myself is, “What happened to all that money that would’ve been spent on travel & tourism?” COVID-19 didn’t destroy people’s money, it merely stopped people from traveling.

Transference

The quickest & easiest answer is to ask yourself how your spending changed as a result of COVID-19, because you probably did pretty much what everyone else did. Nevertheless, let’s look at a survey that was done. Almost 1,600 people responded to this survey and they were allowed to provide multiple responses, so the total adds to more than 100%. In aggregate, the survey shows by percentage of respondents where they re-directed their planned travel funds.

What you can see is that the majority of funds were spent on housing (including home improvements) and big ticket consumer goods. And we wonder why there is a surge in inflation in housing and consumer goods in addition to global supply constraints, when trillions of dollars are re-directed simultaneously into a small number of industries? This should also serve to confirm that the spending we’ve witnessed is not the beginning of a new inflationary era. Rather, it is a one-off re-direction of saved funds that were formerly earmarked for travel. But that doesn’t stop inflationary strains hitting other industries as the short-term demand surge takes resources away from other places. Think of it as a ripple or wave of inflation traveling across all industries as a result of the COVID-19 stone being dropped in the water and not as a tidal swell of inflation.

Another observation from the above data is just how little was saved (approximately 35%). This shows the human propensity to consume, which is what we have observed via inflation in big ticket consumer goods and property-related spending.

Aggregate spending

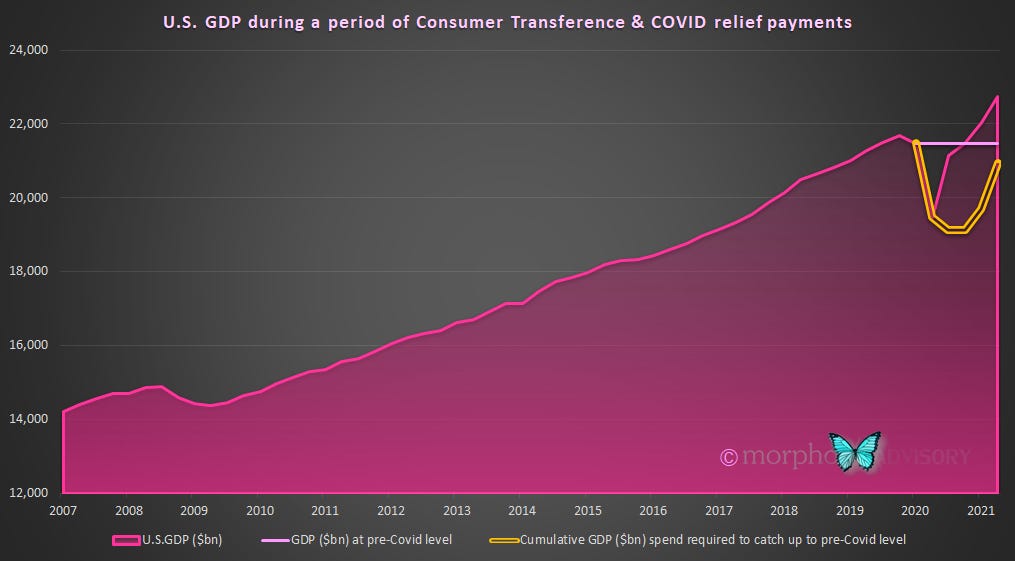

Headline economic data would have us believe that growth is back and that we have returned to “normal”, whatever that is. Certainly, if you look at a chart of U.S. GDP it looks as though economic growth is back to trend. So I asked myself, “Has the GDP that was lost during the COVID-19 crisis of 2020 been caught up?” At the beginning of 2020, U.S. GDP was almost $21.5tn. If we assumed that GDP stayed at this level over the last 18 months (not even grown at trend, but just stayed flat), has the recent surge in GDP caught up that lost activity? Not yet - we’re still playing catch up.

That was just an academic exercise, out of curiosity. The more interesting thought was, “If I take the stimulus (i.e. “stimmy”) injected into the economy by the U.S. Government out of the GDP numbers, what would economic growth look like then? Because that would better reflect the underlying health of the economy.”

That paints a whole new picture of the economy. The recovery doesn’t look quite so good when you remove $3tn in free money given to households (a one-time gift that now exists as an obligation on the current & future taxpaying population as debt). In creating the above chart it reminded me of what Consumer Sentiment data is saying.

Consumer Sentiment fell as a result of the COVID-19 crisis and, although it has recovered some, it is still significantly lower than pre-crisis … and now looks to be weakening again. This gives credence to my adjusted GDP (i.e. removing the COVID relief payments) as indicating the true picture of the underlying health of the economy. Consumer Sentiment has historically proven to be a good guide of the economy.

Ch-ch-ch-ch-changes

It is said that people don’t like change. I disagree. I think people don’t mind change. What they don’t like is change when it happens too fast, and that is what happened as a result of the COVID-19 outbreak. People managed to adapt reasonably quickly. Unfortunately, people mostly adapted by doing the same thing as everyone else, resulting in a bottleneck in our global supply chains. The situation is not unlike markets, which operate well during periods of activity best described as Business As Usual. It’s when everyone heads for the door at the same time in markets, as they inevitably do, that things turn pear-shaped quickly and we experience “liquidity events”.

The economy is going through its own version of a liquidity event as trillions of dollars of travel funds are simultaneously re-directed into purchasing vehicles (e.g. cars, boats, motorcycles, bicycles etc.) and property related spending. The size and speed of the shift has been, and for the moment continues to be, a challenge for the global economy, which has been at a point of stable equilibrium for the last decade.

This too shall pass

In the meantime, the prevailing interpretation of supply chain constraints and inflation is that the economy is strong. So strong, in fact, that plans to remove stimulus are underway around the globe. In reality, it’s not new spending, just spending that is playing catch-up and being re-directed to places unprepared for it. The only new spending was Government handouts that are now a thing of the past. So, despite headline data that suggests all is tickety-boo, things haven’t got better (or too much worse either) - they’re just different. But that doesn’t take into account the shrinking workforce, which was the subject of my last article.

Don’t allow yourself to get distracted by the prevailing headline-based thinking, media noise and your surrounding environment. It could prove expensive.