Static economy

50 shades of white noise

I have been at pains over the last 4 years here on Substack, to point out that the realm of financial markets and economics is noisy. In fact, it is so consistently noisy that the entire professional money management industry has conflated prevailing narrative as determining investment outcomes.

And not only does the industry fill their ears with noise, they let their vision be overcome by noise also. They let prevailing sentiment (as observed via market price action) further confuse them.

We have seen dramatic swings in the stock market over recent times and we have also been bombarded with narrative. For all this, nothing has fundamentally changed in the real economy. Certainly, there are big changes afoot, most notably the United States of America deciding to become a less influential player in both global economics and politics going forward. But for most people, that’s government stuff and doesn’t really come into the everyday activities of their household.

Getting back to basics, the economy across the developed world is primarily people buying houses to live in. They borrow money to acquire these high value assets, which exposes them to fluctuations in the cost of money. When inflation rises, central banks raise interest rates to cool economic activity. That’s exactly what has happened over recent years.

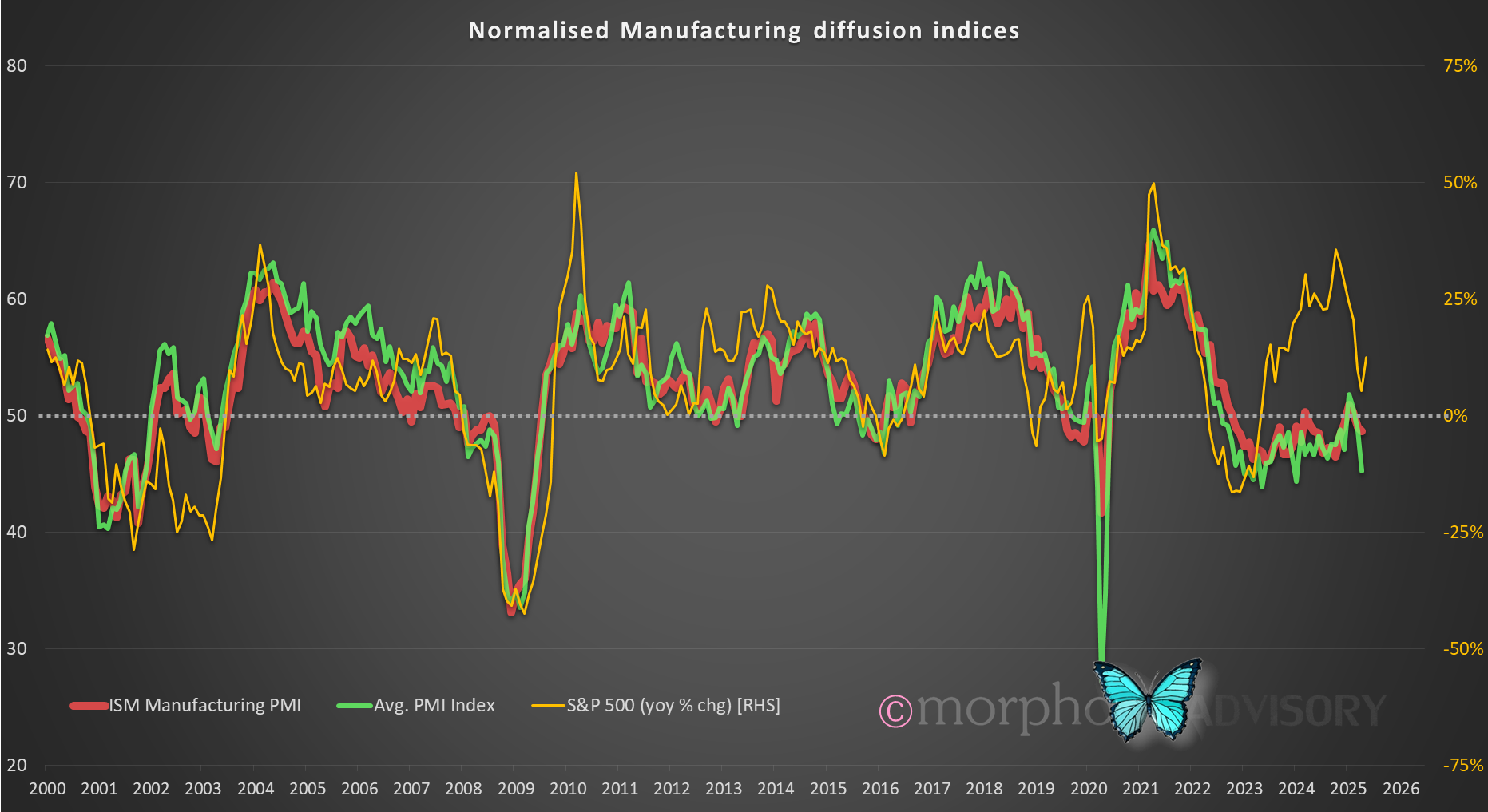

The following chart is a diffusion index and shows the activity in the U.S. manufacturing sector. When the score is below 50 it means that activity is slowing, and above 50 means it is growing. You can see that large falls in activity typically coincide with recessions.

For the last 2.5 years, the U.S. economy has been static (not just the noisy variety, but the “at a standstill” variety, too). Manufacturing activity has stalled and actually been contracting. Only recently did it briefly pop back up into growth territory. That brief spike up above 50 at the beginning of 2025 was a lot of activity being done before tariffs were introduced by the new president. Since then, normal business has resumed, i.e. less business.

So, you can see, the economic slowdown of the last 2.5 years is not really driven by politicians (just as economic growth is not caused by politicians). It is households and businesses having less free cash flow because the cost of servicing their debt has risen.

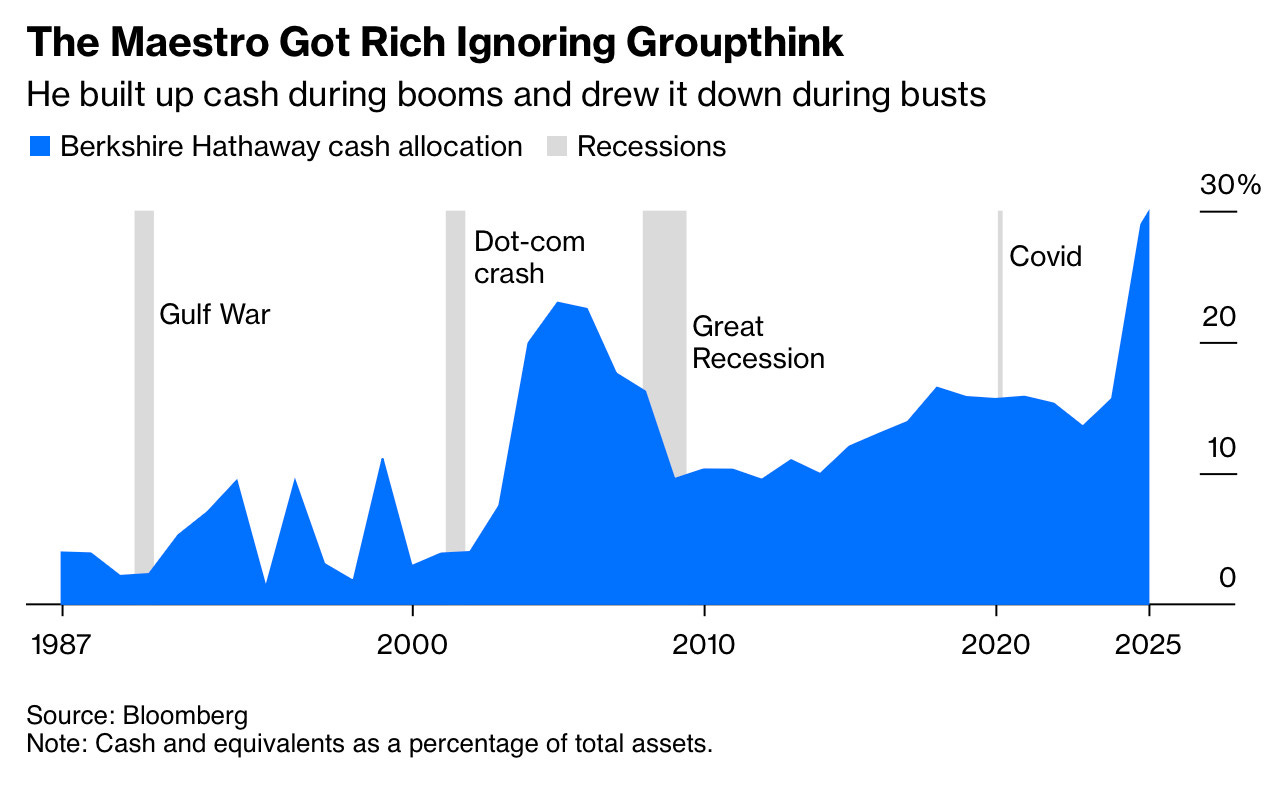

The retirement of Warren Buffett as CEO of Berkshire Hathaway has been well publicized recently. Mr. Buffett (along with his long time partner Charlie Munger) have been exceptional investors, far exceeding passive index investments. They made their investment decisions by looking at the cash that is generated by businesses. They shunned the Wall St. approach of noisy narratives and swinging sentiment. When there was no cash generating businesses that took their interest, they simply parked their cash until there was. That’s why Berkshire Hathaway has a record amount of their capital sitting in cash at present.

The large rise in interest rates of the last few years is having an impact on household cash flows (i.e. squeezing them), which feeds into business cash flows.

Why has the stock market risen then? Euphoria, mostly. People want to believe and they’ll latch on to any story that lets the dream continue: AI? It’ll change the world. Buy!

The chart above is the same as the one at the top of this article, but it has the annual return of the S&P 500 Index overlaid. Here, we clearly see how the stock market has deviated from the underlying economy over the last 2 years. The stocks in S&P 500 (particularly the top dozen or so) have not been going up because their cash flows are going up, they’ve been going up because of - using the technical jargon - “multiple expansion”. That simply means that people are paying more for less in hopes that the price keeps going up and they become rich.

The last 2 years has been when Mr. Buffett decided that business cash flows don’t match the market price and has been selling equities and holding cash. He and Charlie Munger have done this successfully for 6 decades.