This time is different

Mmmm .... okay

Happy Anniversary

It’s almost 2-years since my first post (12 June 2021) here on Substack! Only a month later in July 2021, I forecast a U.S. recession in 2023 (with the possibility of it starting even as early as 2022). This was at the height of BTFD, cryptomania, the great resignation and a flood of new entrants who were going to make their way as day traders. Good times.

I was the voice of one crying alone in the wilderness.

Which just goes to show how slow economic cycles are and why quality economic and finance-related content is contrary to the infotainment world of social media.

Oh my Stars and Garters!

I’m seeing people declare that recession has been priced in and that the worst is behind us. And not just any people, but names that have put themselves out there as experienced playas in the global macro scene. Some of these people have massive followings in the online financial-sphere.

Ordinarily, I would be happy at such news because when there are punters who have a contrary view, then there is less chance of the market being heavily skewed (e.g. like everyone being ‘short’ in the middle of last year only for a 12-month slow squeeze to occur [yep, I had a small short that I closed out, too]). However, it’s the following that these people have that concerns me, which I think may have tilted the perception of all involved. The followers know no different and so accept whatever they’re told, thinking they’re getting the ‘goods’ and the charts appear to tell a story. And the experienced playas feel compelled to engage their audience and so produce regular output. But this is the same problem that mainstream media face - it’s hard to produce meaningful output (especially in relation to economics, which is very slow moving) on a daily basis, and that leads to: a). a drift toward sentiment and price action based content, and b) the cult of personality. As a result, these “names” have moved away from consistently robust indicators to more recent ones, and that is tantamount to saying, “THIS TIME IS DIFFERENT” - the ultimate market sin.

That moment when everything seems clearest to you usually means that you’re at the top of the mountain … your view is unimpeded … but the only way is down.

Last August, I asked you all to reflect on what your personal financial circumstances were like. I hope you still remember your reflections from that time. If not, maybe scroll back down your Instagram, Facebook or whatever app you use to refresh your memory of where you (and your thinking) were at back then. I’m asking you to do it again now. I want you to create a series of mental markers, so that you have reference points for future use.

Shit’s about to get real

Ladies and gentlemen, we are in it! In fact, we may have been in recession as early as the end of last year. Pretty unremarkable so far, huh? Personally, I thought the fireworks would’ve started before now, but I was wrong … probably because this has been the most anticipated recession in history. But that only delays the inevitable - possibly even making the ultimate washout all the more spectacular?

Interesting fact: the U.S. recession that started in December 2007 was declared by NBER in December 2008.

I showed in my last post that the peak in year-over-year inflation (pink line) usually aligns with a recession (vertical shading), either right at the beginning or about mid-way through. In the current cycle, that was June 2022.

I also showed that the stock market usually only falls in earnest after interest rates are dropped by the Fed, i.e. upon confirmation that the economy is in the shit. So much for a pivot being positive.

We haven’t pulled out the yield curve in a while. Let’s take a look.

The current super-low inverted yield curve (itself inverted in the above chart) is warning of risk that investors are ignoring … and with the peak in inflation already in, plus inflation dropping rapidly throughout the remainder of the year, the Fed will begin to think about the state of the economy …

What is that state?

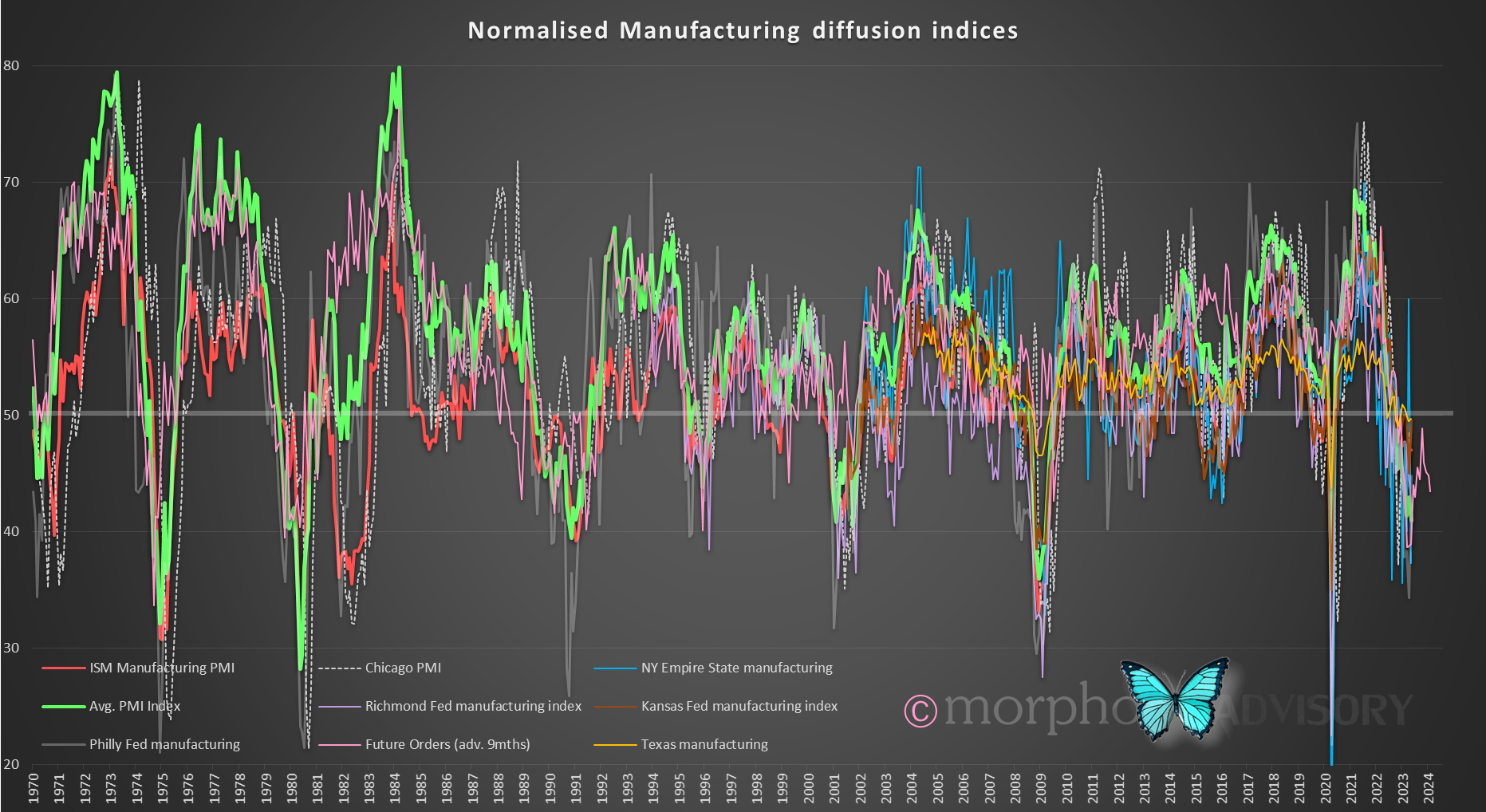

Manufacturing is not looking good, with every regional survey being ‘below the line’, and that don’t happen often.

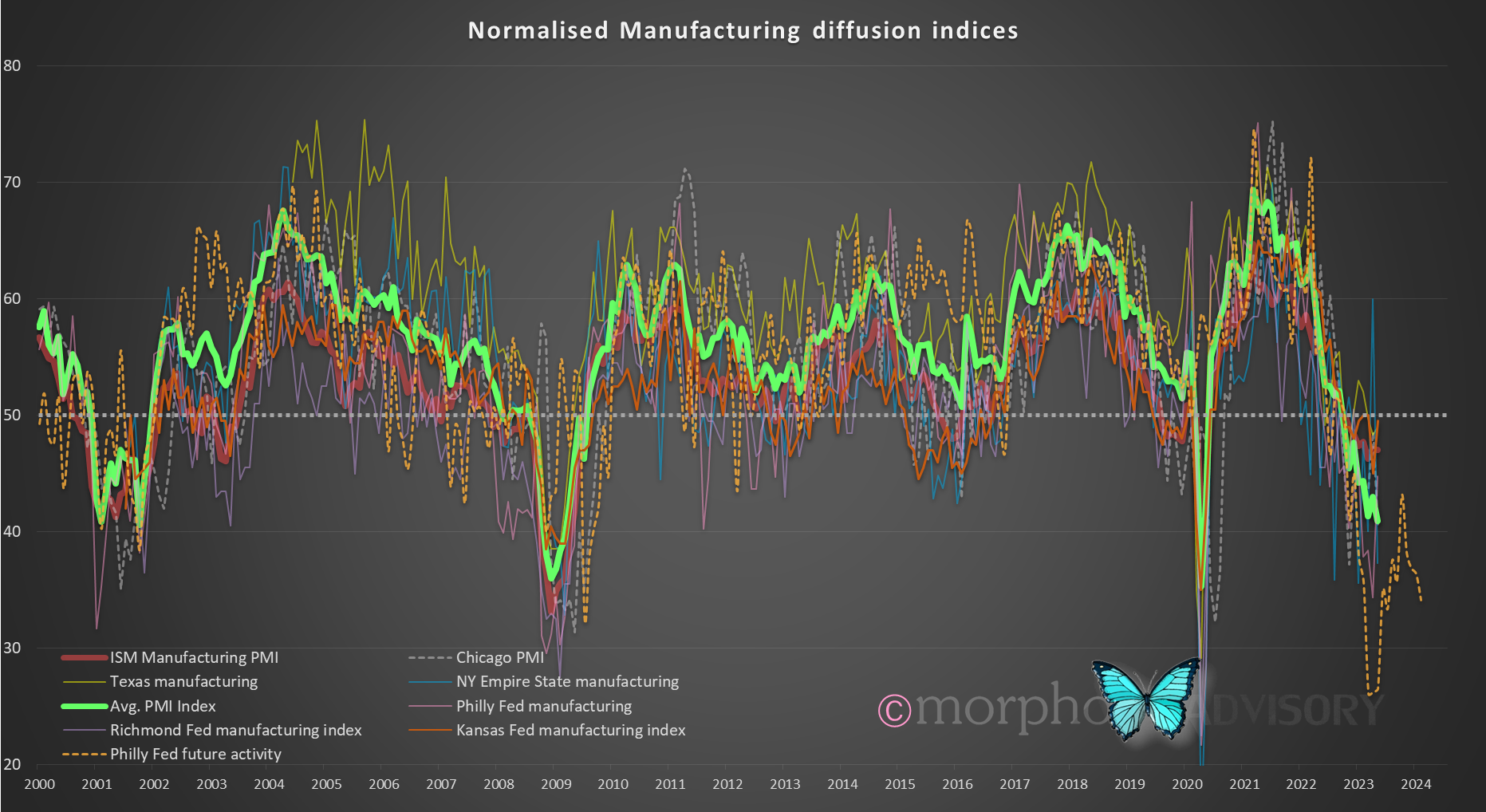

A close up of the last 20+ years with a peek at a forward indicator suggests a prolonged lull in manufacturing activity, which correlates to both GDP growth and stock market returns.

Employment has been the sticking point in the current cycle, at least from the point of view of the Fed who use it as a sign of a strong economy, so they’re gonna keep sticking it to inflation.

Low unemployment is NOT a sign of a strong economy. It’s the other way around. A strong economy creates low unemployment, but Recession is what changes that and sends the unemployment rate higher.

Year-over-year data tells the real story … and labor markets are dropping.

Other indicators, like job cuts, continuing claims etc., are all turning, too.

Retail sales, which reflect both the consumer and corporate earnings, is not looking resilient. That is especially so when you take into account the impact of inflation eroding what a dollar buys. The dollars spent may be up, but volumes sold and therefore profit margins made, are lower.

So, you still wanna buy this market believing that the worst is either behind us or recession is ‘priced in’, or that liquidity will save the day?

The year-long lull in the market is beguiling. However, it’s almost time to act against the prevailing sentiment. If I had this time (the last year) again I would do things differently, but I’m wiser now - always learning. That’s the point of this website. Over 30 years in markets and I’m always looking for ways to improve.

I’m looking forward to this opportunity, really looking forward to it.