Your Investment Portfolio is Religious Dogma

Simplistic risk profiles make you believe it's a personalized service

You’ve been sold a faith not a solution. From financial regulators down to financial advisers, your investment portfolio is the product of their collective adherence to a erroneous and fanatical creed. Thinking is only permitted within the confines of the Articles of Faith. Thinking beyond the cult’s framework risks excommunication as a pariah because regulators demand certified indoctrination. Ultimately, the evangelical expression of this religion is selling. Selling pre-packaged religious artifacts is the name of the game.

What am I getting at? I’m saying that no thought goes into investing your money. Sure, there’s some thought, but it’s not real thinking. Let’s look at it from first principles.

Why do you invest?

To make your money grow - to have a greater relative value in the future, i.e. more spending power than you do today.

What obstacles would prevent that from happening?

Losses.

So, in summary, we want to invest in a manner that grows your wealth, but also actively limits losses along the way?

Yes. And that active risk limitation is important because we don’t know when losses might occur. If they happen just before the money is required in the future the outcome could be personally catastrophic.

From an investor’s perspective it’s a fairly simple proposition. But that’s not how the financial industry approaches it. They skip that ‘what the customer wants’ bit and go straight to selling their mass-produced shrink-wrapped shiny indulgence, which they can show as being better than the shiny indulgence sold by that other congregation on the other side of town.

How is your investment portfolio built - the one that was sold to you?

You’re asked (or maybe you’re told based on your age) what “risk” you can tolerate. Can you live with the value of your investment dropping from time-to-time, and by how much? From this you are profiled as a Conservative, Balanced or Growth investor.

At the Conservative end of the spectrum your money is invested mostly in fixed income (bonds) and other income-based investments and less in equities (stocks) and growth-based investments. At the Growth end of the spectrum the opposite is true. And that’s it! That’s the secret recipe. But it’s an ill-considered and fundamentally flawed model.

How is this model flawed?

It does little to actively manage the risk of loss, plus it reduces the performance of the investment in the process. It essentially fails on the two primary principles of investing: (i) risk; and (ii) return.

From the perspective of the investor, they want to participate in market upside whilst avoiding the downside.

What have you been sold?

Essentially, your investment portfolio is one that drives with the brakes on - your risk profile decides how heavy the foot on the brake is. You wouldn’t drive a car like this, but the investment industry does exactly this with your money. In the process you are carrying unnecessary risk and losing out on investment income.

Let’s explore what you’re investment portfolio looks like.

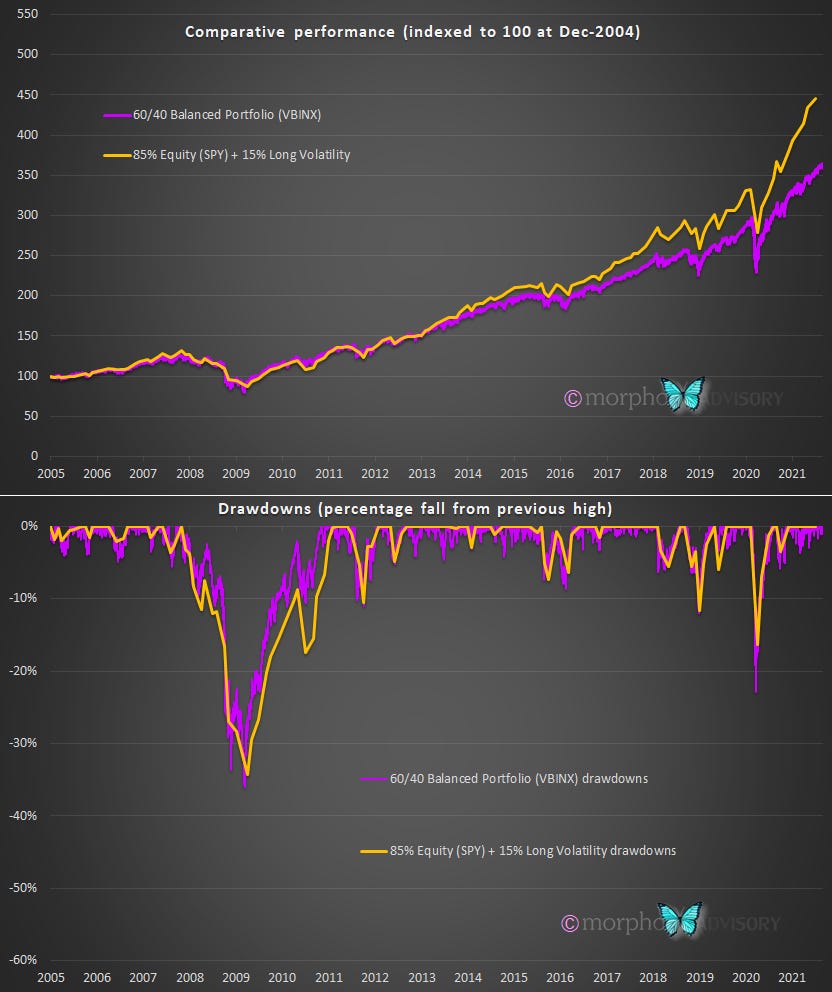

The following charts compare the S&P 500 with a Balanced Portfolio. The Balanced Portfolio is basically a replica of the S&P 500 but with a dampened profile, i.e. not as extreme in terms of market moves to both the upside and the downside.

The comparative drawdowns (periods of losses from previously attained highs) show how having an allocation to fixed income in your portfolio dampens the more extreme losses incurred, but this comes at the cost of lower returns. This trade-off is undoubtedly explained to you when you are sold the investment. But is this the best way of achieving your risk-to-reward goal? No it is not!

You want to barbell your portfolio. One aspect to enable you to participate in market moves higher giving your portfolio its returns without being held back. The other aspect lets you achieve your risk management objective. Can this be done? Yes it can, but there’s a catch. The catch is that it requires a professional to arrange this structure (i.e. the risk management aspect), which compounds the frustration because the professionals are the ones with their head in the sand about these things - too busy selling to actually think what is best for their clients.

Anyhow, here’s the approach that the investing industry should be adopting as a matter of course. To get higher investment returns they should invest in the stock market (equities). To manage market risk, they should invest in volatility through a Long Volatility fund. This simple approach gives participation in markets while providing superior risk management.

The following chart compares the equity/long volatility barbell portfolio with a Balanced Portfolio. In this example the relative weight of equities to long volatility has been calculated to achieve the same risk profile as the Balanced Portfolio based on drawdowns. As you can see, the return of the barbell portfolio is superior to the Balanced Portfolio for the same level of risk.

In the following chart, the relative weight of equities to long volatility has been calculated to achieve the same return as the Balanced Portfolio. As you can see, the risk of the barbell portfolio is much lower than the Balanced Portfolio for the same return.

Whether reducing risk is the main concern or increasing returns, the investment industry is neglecting their duty of care to their clients. They are taking too much risk with their client’s money for too little return … plus they’re charging fees for the privilege!

Why isn’t this barbell approach that utilizes equities and long volatility adopted by the financial industry and investing professionals? Because they don’t apply thought to understanding the mathematics of investing, neither do they understand risk as it pertains to markets in the real world - they tend to use a silly classroom concept of risk. They have unquestioningly adopted the theory they were taught by academics, who themselves are intellectually constrained in their well-studied thinking besides having no practical investing experience to draw upon and so test their theories.

The investing industry are even ignorant of the fact that their pre-packaged solutions will get worse. With interest rates near zero percent (and below zero in certain places) the fixed income element of their portfolios will not provide any return on investment let alone offer the dampening impact it has provided over many prior decades. But the industry persists in rolling out its dogma-based portfolios because there is money to be made running their investment machine and there’s no time to think.

They blindly follow the academic theory and its “small allocation to everything” model believing that this is diversification rather than “big allocations to the right things.” They look at Long Volatility as being poor performing (as the following chart suggests) and therefore not something to hold in their portfolio - “it’s too expensive” - rather than seeing all the allocations that they hold that are not to equities. Everything that is not to a robust growth investment like equities will drag investment returns down so it better compensate at the portfolio level in terms of risk.

When combined intelligently, a well constructed portfolio improves both the investment returns and reduces the risk of loss. But this requires real-world intelligence in an industry shaped by and controlled by classroom intelligence.

Classroom intelligence has no understanding of risk in the real world. It also (apparently) seems to miss the fact that’s it’s not just what you add to a portfolio, but what you take away, that makes all the difference.

But what do I know? I’m just a heretic.