What up, Homies?

I thought I would do a quick wrap of my writing for the year because my thinking vis-a-vis the economy was spread across numerous articles and I know you didn’t go back and read them all to build yourself a cohesive view. I’m a little disappointed in y’all, but it is what it is. So here goes, all quick and dirty:

The economy is about people, not policy

Starting from first principles, the economy is a subset of society. That is an important concept that most forget - even at the highest level. Economics is merely the financial aspect of human interaction.

When we start from that fundamental position it is easy to understand that when society grows (i.e. population-wise) then the economy grows.

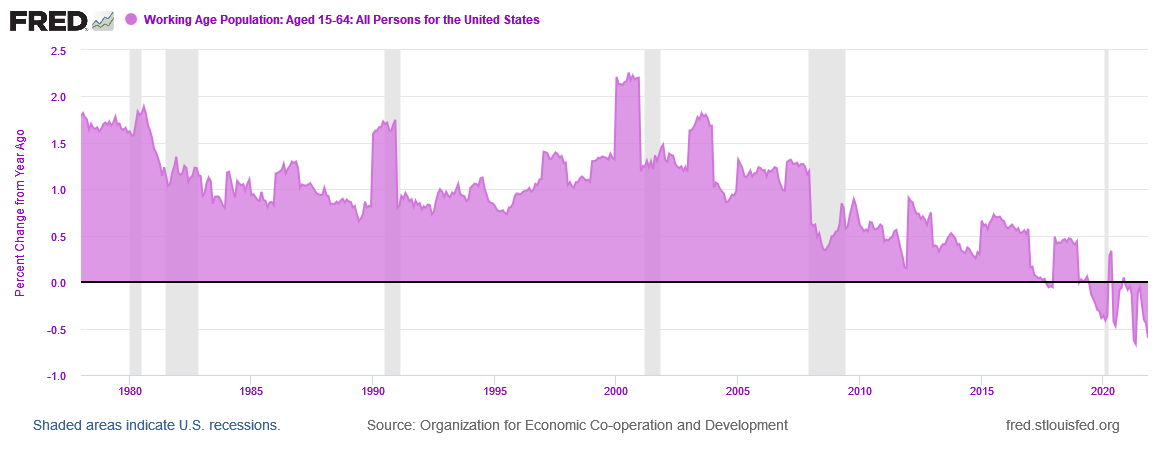

We can see this facet at work during the middle of last century. Post-WWII, people started making babies in earnest and so we had the Baby Boomer generation. These Boomers started coming of age around 1960, which is when they left school and started working. At that time, the U.S. economy was comprised of 100 million workers. By 1985 there were 145 million workers. That’s a 45% increase. The economy of the 1960s was not prepared to absorb 45 million extra people and so it experienced growing pains, which was observable via higher unemployment and inflation.

By 1985, the economy had finally adapted to the necessary expansionary mode required to absorb additional labor resources (i.e. money was flowing freely through the economy so businesses were in a position to hire people at will - a luxury that didn’t exist in the early days of the Boomers, hence the subsequent inflation).

From 1985 until the GFC in 2008, the economy added another 45 million people without problem, taking the Working Age Population up to 190 million people. However, this time those additional 45 million people were only a 31% increase compared to the 45% increase between 1960 and 1985. I point this out because economic activity is measured in terms of its growth rate as a percentage. It also illustrates the mathematics of diminishing returns (e.g. 45/100 is not the same as 45/145 - the denominator is important).

The chart above compares the U.S. Working Age Population against the Total Population. It shows the growing pains during the 1970s as the Working Population vacillated relative to the Total Population. From 1985, the population bubble that is the Baby Boomers (followed by the Millennials from the mid-1990s) has seen the Working Age Population as a disproportionately larger component of Total Population than other times over the last 60 years. At this point I should note that I focus on Working Age Population because they are the driver of the economy - they work, they earn, they spend.

Here’s another key aspect of economics. It is a zero-sum game1. If we recall our first principles statement that economics is merely the financial component of society and add it to our understanding that the economy expands organically as the population expands, we realize that everyone who is born will die. A population bubble is great for economic growth during the expansion phase, but what about when that population bubble deflates?

The Working Age Population in the U.S. is now shrinking. As I have demonstrated in earlier posts, this trend is likely to continue into the 2030s.

Regulating economic cycles

If economics is not about policy, then how will markets regulate? Before continuing, I should say that despite economics not being fundamentally about policy, policy can and does shape the way the economy travels from A to B so policy frameworks need to be taken into account.

For the most part, economics has this funny way of sorting itself out. Natural monopolies are the main exception and these should be regulated. Remember, economics is a human interaction. If people don’t like the price, they can choose not to transact or they can find an alternative.

Certainly, there are times when elements of economics get way out of line and many are hurt by the subsequent fallout. But is it better to have smaller exposure to more frequent such actions than suffer massive failures because a regulatory body has suppressed the necessary learning experience that comes from normal human actions that stem from allowing fear (including FOMO) and greed to govern economic choices?

Let’s have a nosey at a few enlightening charts to see self-regulating markets at work.

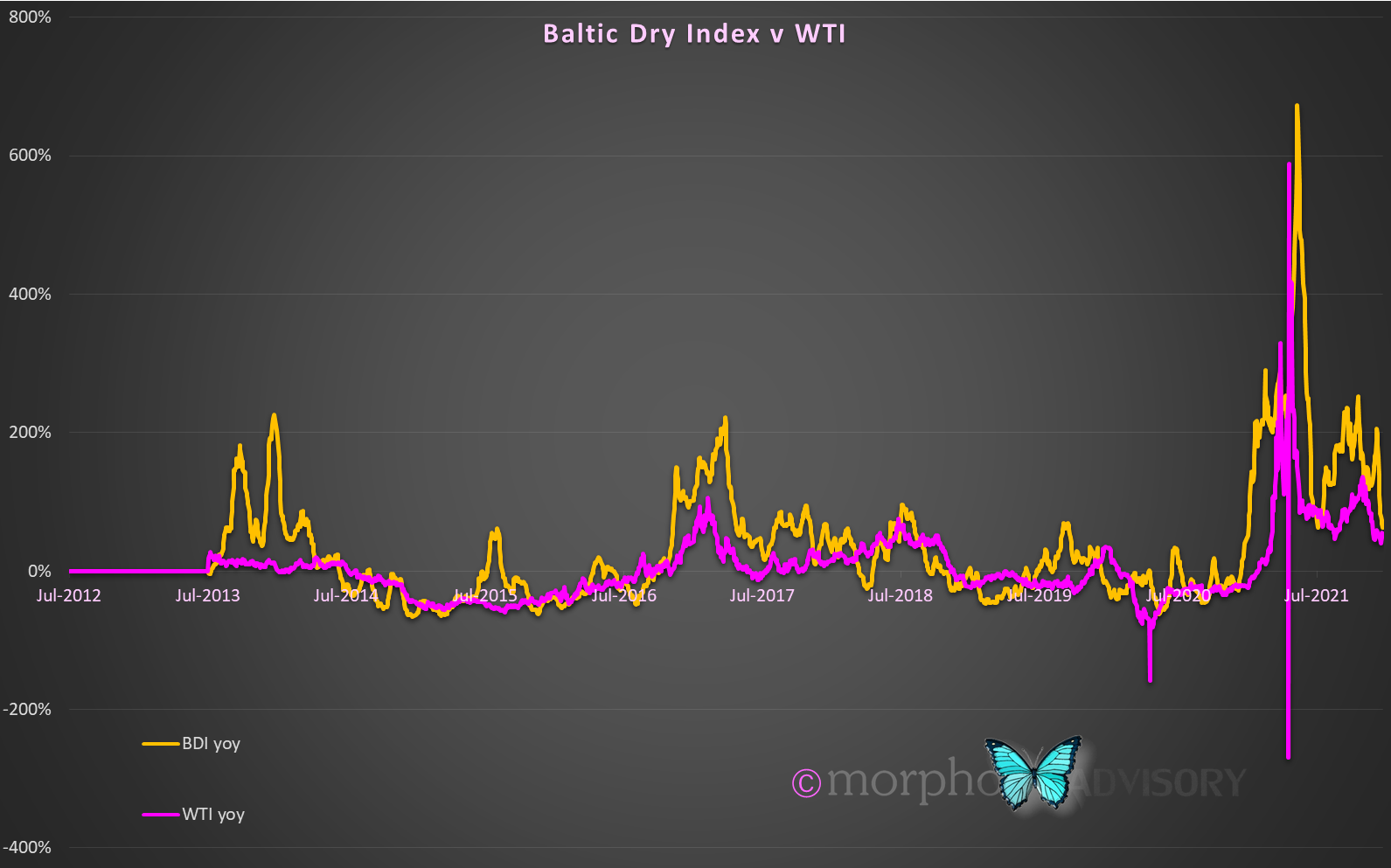

As we all know, inflation is the concern of the hour and the Fed is psyching itself up to to be the Big Swinging Dick and bring it under control. However, I have previously pointed out the correlation between inflation and the price of crude oil, which appears to be on its way to settling back down … and this of course, implies inflation will follow suit.

The reason that the price of oil spiked was due to a spike in economic activity, which can be seen in the price of international shipping, as measured by the Baltic Dry Index … whose prices moves correlate to the price moves in oil.

What these charts also show is that the growth rate does not continue ever higher (I don’t care what the prevailing narrative is saying, e.g. that we’re going “to infinity and beyond”). There always comes a point when price forces a reduction in economic activity, because people have a limit that they are prepared to pay, or can pay.

So what’s the point of the Fed?

Now you’re asking the right questions!

Economic policy and financial regulation are more often than not an attempt to fight yesterday’s battles today.

If we look at the supply-side economic policy and Federal Reserve inflation targeting of the last four decades we see a system designed to keep inflation under control, because that was a significant problem between the mid-1960s and mid-1980s. As mentioned above, the inflation of that time was due to an economy that needed to expand to accommodate a growing population and it struggled to do so.

These government agency actions were implemented just as the problem had sorted itself out. In the case of the Fed, they were left to use interest rates as a means to keep the economy ticking over at their ‘new normal’ assessment of sustainable economic growth sans-inflation, but which in hindsight was anything but normal levels of economic growth. As a result, they have induced a surfeit of system-wide debt (household debt + corporate debt = 125% of GDP). As that experiment has failed, they having used up all their interest rate setting lever by hitting the lower bound (i.e. zero), instead of taking an objective view as laid out in this article, they jumped straight into quantitative easing, because that is what their Japanese peers did and they felt compelled to do something even while they were building up a track record of QE not working to achieve their desired objectives. QE has resulted in Federal debt exceeding GDP (also at 125% of GDP) plus massive financial asset speculation, and this is occurring just as Working Age Population growth is turning negative for an extended period with its implied economic consequences for the next decade (e.g. low/no growth; low/no inflation; greater government outgoings via pensions; lower government revenues via a smaller tax take; more government [taxpayer financed] debt etc.).

In summary, bureaucrats and bureaucratic agencies have a history of exacerbating problems rather than - as they are employed/created to do - resolve problems.

Is economics really that simple? Yes. Only, we humans often feel a need to make things more complex than they are, plus we only accept knowledge from academics who love the abstract and the tangential. Additionally, policy and regulatory oversight requires the sort of discipline that a bureaucrat doesn’t possess - to take their hand off the wheel - especially when the clamor of opinion about what they should be doing rises and politicians who demand to be seen in a good light hold the power of their job. All the incentives are short-term (e.g. over business/election cycles) in a field that needs to have a long-term perspective (e.g. over multi-generational life cycles).

Happy New Year!

Money simply passes from one person to another. Oh I agree, the economy can create the illusion of expanding wealth for all, but it is just an illusion. Take property as an example. Only 5% of properties are on the market at one time. As they sell at higher prices, everybody’s property is marked higher in value by interpolation. This makes people feel wealthy and so they borrow more and spend more etc. But if we look at financial markets during crashes, we see everyone trying to sell stocks at the same time, prices dropping and trillions wiped of market value. This is called a “liquidity event” because there are not enough buyers to meet selling demand and so the market is forced to shut. Wealth is an illusion as long as it is not realized (i.e. cash in the bank). While it is still a financial asset it is subject to the vagaries of market fluctuations.

And don’t get sucked into believing that productivity will create wealth, it merely redistributes it to the most efficient part of the economy.