Double dipping is poor form, but it still happens

First you need to untangle your thinking from the COVID-19 economic head fake

There is much confusion going around in relation to markets and the economy. Inflation data is soaring while bond yields are falling and the majority of financial pundits - especially the many social media market “experts” - are opining in a manner that seems to confuse the size of the jump in inflation with the likely duration of this jump in inflation. Even chair of the Board of Governors of the U.S. Federal Reserve, Jerome Powell, confessed to not understanding the behavior of bond markets in the face of strong inflation, which merely confirms my estimation of the capability within key financial institutions. Like every social media market pundit he is thinking too short-term and not seeing the big picture - this, despite it being his job.

NOTE: I would suggest taking the view of the bond market over the opinions of any other sort of expert (trained or otherwise). The bond market is the only expert whose income is dependent on being right about these things - and they have a good track record.

As someone with two decades seeing the world as a fixed income asset manager (bond buyer) and another decade as fixed income liability manager (bond issuer), I’ll summarize the world as I see it, which seems to reflect what is happening in the bond market at present. To make it simple, I’ll put it in bullet points:

the global economy started slowing at the end of 2018 (i.e. we were heading toward recession one way or another);

trade wars accelerated the economic slowdown - recession was a done deal;

COVID-19 was the catalyst we were waiting for … only it didn’t happen the way it was meant to. COVID-19 was so huge - stopping the global economy in its tracks in an instant - that governments just threw enormous amounts of money at everyone without having the time to quantify how much was needed. The result was that people’s incomes actually went up during a recession for the first time ever. This had multiple effects:

lockdowns meant people couldn’t spend their money so it caused pent-up demand (i.e. money just sitting, waiting to be spent);

businesses ran their stock down to reduce the cost of staying in business while their income was down severely;

in summary, it was a supply recession - there was still demand, but people couldn’t get out to spend. A traditional recession is a demand recession, i.e. times are hard so people cut back on their spending;

additionally, people were being paid more to stay home than they used to get from working. When you combine this with people now living online, it led people to take up online day-trading. Central bank QE underpinned equity markets making speculative trading easy money. New careers were launched.

economies re-opened and, with all that money just sitting there, shopping resumed in earnest, but showroom stock was low so people competed for available goods and the sellers raised the price to reflect this competition;

companies found that post-COVID-19 supply chains could no longer supply goods at the pace they could pre-COVID-19, so people competed for available goods and the sellers raised their price to reflect this competition;

people began working online (remotely) and, with interest rates having dropped to zero, they could buy a house out of the city to gain quality of life, so people competed for available houses and the sellers raised their price to reflect this competition;

people are still being paid to not work (and are making more money through their seemingly risk-free trading activities [an unintended consequence of QE]). Businesses that laid off staff when COVID-19 hit can’t find employees, so they are competing for available workers and have raised their price to reflect this competition.

It’s easy to see why there is inflation. Government and central banks have removed all the pricing signals. Fiscal stimulus (“stimmy”) encourages people to not work and yet feel wealthy, whilst low interest rates plus quantitative easing (“QE”) encourage people to speculate on asset prices. Consumer demand has returned instantaneously post-lockdown, but supply chains can’t respond at the same speed, even though the underlying productive capacity to meet demand is available. That’s what the bond market sees. There is a lag, but give it time and goods will be available to meet demand again. But the bond market also sees something else.

Once you remove government intervention, the underlying economic situation is still below what it was. Remember that weakening economy pre-COVID-19? Well, post-lockdown, unemployment is higher at approximately 6% compared to 3.5% prior. The demographics associated with an aging population is also putting long-term downward pressure on economic growth. And last, but not least, we are now in a tightening cycle.

Yes, that’s right - a tightening cycle. There is an adage in the commodities sector that goes something like:

“The cure for high prices is high prices.”

It means that there is a self-regulating mechanism inherent in human behavior. All those rising prices, as described above, encourage businesses to produce more so as to profit from these high prices. But producing more, once the immediate demand is filled, then causes oversupply, leading to falling prices. There is another aspect to it, which explains why I say we are in a tightening cycle. The current monetary policy framework is based on inflation targeting. This means that the relationship between inflation and official interest rates is very strong. However, with an underlying downward trajectory for economic growth, central banks can’t raise interest rates. But don’t worry, inflation is doing the work of the Fed at present. Inflation is doing the same work as rising interest rates. It is taking away disposable income from people. Instead of making borrowing more expensive, it is making consumption of goods and services more expensive. To illustrate my point, look at the following chart in which I compare the Effective Federal Funds rate with a combination of the Fed Funds rate and the Consumer Price Index (“CPI”). In this chart I have halved the CPI (multiplied by 0.5) and added it to the Fed Funds rate multiplied by 0.7 (I was trying to average the two to show how their combined impact is the same as Fed monetary policy). This combination got the historic relationship the closest. If you look at the right-most point of the chart it shows that the current spike in CPI is the same as if the Fed had raised their Fed Funds rate to 2.7%. That’s 2.65% higher than where the Effective Fed Funds rate currently sits and equal to the highest point of the Fed’s tightening cycle that ended in 2019. Hence, “we are in a tightening cycle.” Oh, and the bond market saw this inflation coming and began moving bond yields higher from August 2020 through to March-May of 2021. Now they see through the other side of the COVID-19 impact and the old cycles resuming. Besides, any tightening cycle inevitably leads to an economic slowdown.

Yep, this whole COVID-19 situation is one massive economic head fake. It got people thinking “catastrophe” only to deliver a huge surge in growth. Now it has people thinking “new cycle of economic growth” only for it again being a gigantic magician’s act of misdirection that has us looking in the wrong place at the right time.

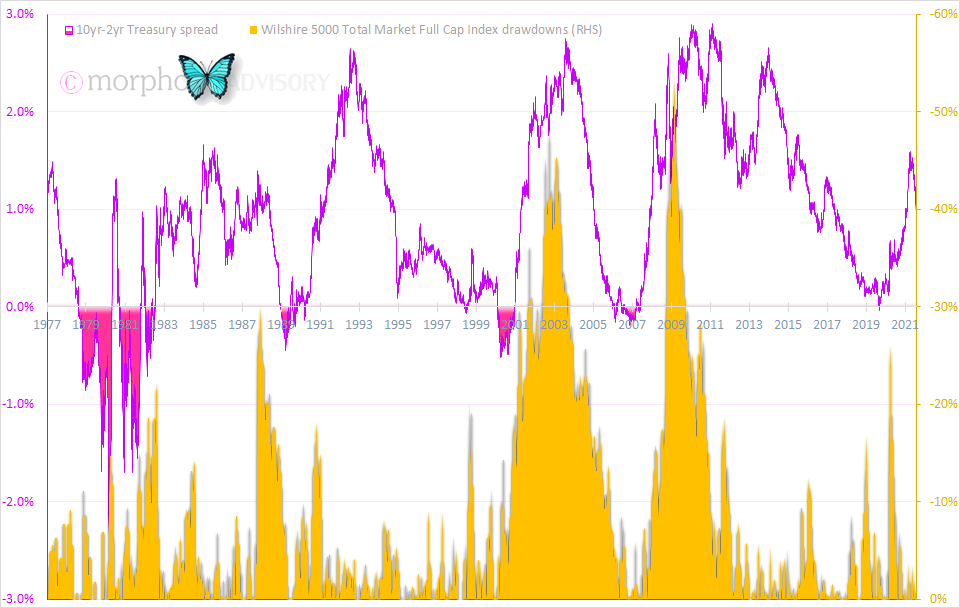

And that brings me back to the idea of double dipping. I’m talking of a double dip recession, which I think is still very much on the cards. I’m thinking 2023-ish+/-. My earlier publications include charts illustrating the relationship of economic growth to demographics, which suggest flat to negative GDP growth over the coming decade. But the yield curve has me questioning things also. The yield curve refers to the relationship between interest rates at different maturities (e.g. 2 years; 10 years; 30 years etc.). Historically, the spread between the 10 year U.S. Treasury yield and the 2 year U.S. Treasury yield has been a good indicator of an economic downturn and corresponding market sell-off. When this spread has gone negative it has presaged such an event, as illustrated in the following chart.

The 10 year-2 year spread is not currently indicating such an event. But I want to show you how a bond portfolio manager thinks (just as I have shown above how they think of the current economic situation) about these indicators, which have become common lore amongst money managers who then think no further. I thought, “With interest rates being so close to zero, it would get increasingly difficult for the 10 year yield to maintain its historic relationship to the 2 year yield.” As such, I asked myself if there is a more valid way to assess this relationship in the current environment? Oh, I should explain. What this spread shows is the long-term economic outlook relative to the short-term economic outlook. A negative spread means the long-term outlook is weaker than the short-term outlook and this is what I expect to see in the not too distant future once the current spike in inflation is excreted from the 10 year yield. Anyhow, I came up with an idea that verified my suspicion (i.e. that the 10 year-2 year spread is losing its veracity as a signal now that interest rates have approached zero). My idea also proved valid in that it has maintained the accuracy of the historic relationship whilst also making current signals more meaningful in a low interest rate environment. What I did was I assessed the spread between the 10 year and 2 year U.S. Treasury yield with the spread between the 30 year and 10 year U.S. Treasury yield. This method also shows that it is common for the yield curve to experience two periods of a negative spread prior to economic and market downturns. The current cycle has only experienced its first, as you can see in the following chart.

In this current cycle, the COVID-19 impact reminds me of the late ‘90s when the 1997 Asian Crisis and 1998 Russian Crisis led to the collapse of LTCM. This caused market tremors, but any more significant impact was averted because the Fed organized a bailout …“Yay! Everything is fine.” … only for the Dot-com bubble to burst a couple years later. Oh dear.1

At present we have the majority of market strategists talking of reflation trades plus positivity from re-opening economies and vaccination rollouts etc. These are valid positive short-term economic events and these people are paid to think short-term and produce regular output (e.g. daily, weekly etc.). However, in relation to all the positivity about at present I am reminded of the New Testament verse 1 Thessalonians 5:3, which says:

“When people say, ‘There is peace and security,’ destruction will strike them as suddenly as labor pains come to a pregnant woman, and they will not be able to escape.”2

I am reminded of this not because I am a Debby Downer per se, albeit bond managers are ever on the lookout for risk. It is because I see the current environment within the context of a larger movement. The main risk to my outlook is a continued disconnect between the economy and financial markets as the Fed continues to grow its QE program, plus continued Federal Government stimmy. These I see as potentially deferring the coming downturn rather than avoiding it. [NOTE: see comment section]

Anyhow, that’s the bond manager perspective. We think big picture and have long-term outlooks that underlie medium-term strategies and short-term tactics. The reason that Jerome Powell (and most others) can’t understand falling bond yields in the face of spiking inflation shows a lack of comprehension of the big picture and the longer-term - the very one he is supposed to be in charge of managing. Go figure.

Some might say these things were unrelated, but they were - I just can’t share it because it forms part of my proprietary methodology.

International Standard Version

Here we are less than 2 days after I published this article and I have already altered my view from what is written above, but only slightly. This why you need to develop your own view on the economy & markets rather than relying on others to form it for you. Unless you are paying someone else for the privilege, portfolio managers & other market professionals (like myself) can change their view in an instant and they are under no obligation to update you on their changed outlook. This is what I was taught in my earliest days in the market - you've got to have a view.

So, what's changed? Just like I said in the article, that stimmy & QE could prolong the time until the coming downturn, the current tightening cycle caused by the spike in CPI can hasten the downturn. How so? A Fed induced tightening cycle via raising interest rates takes time to fully impact the economy because most households & companies have fixed rate loans. So, only when the current fixed rate period expires will loans be reset at the now higher interest rates. By comparison, only businesses (and not all of them) have fixed cost supply contracts. As such, a CPI induced tightening cycle will hit the economy much faster because all households and many businesses will be hit with higher costs immediately.

Because of this difference, it is possible that a double dip recession and/or significant market fall could happen sooner than the 2023 estimate posted above. This could especially be the case if stimmy stops and QE is tapered etc. Be warned thought, I have been guilty of being early in my timing of calling a recession etc. in the past. For example, I called for one in H2 of 2019 only for it to happen in H1 2020.