The Good Oil on Inflation (Part 1)

Putting some numbers around inflation expectations

[PART 1: INSIGHT - that requires Interpretation and has actionable Implications]

Here’s a quick one for your consideration. These thoughts have been drifting in & out of my mind for a little while, so I finally decided to do some analysis.

My starting position is that: changes in the price of oil is the primary driver of inflation. I’ve posted something that implied this earlier. You may agree or disagree, but here’s some evidence to back up my claim. The following chart compares the U.S. CPI with the annual percentage change in the price crude oil. I applied the following formula to the annual percentage change in the price of oil: I divided the annual percentage change in the price of oil by 20, and I then add 2%. That’s all. I simply scaled it down and then shifted the result up a bit. It makes for a nice match.

Why have I been thinking about this?

Because, I think the global economy is going to start turning to shit in the not too distant future, beginning later this year and possibly as early as August 2022.

Therefore, I am wondering if the current pricing of interest rates & bonds is getting a little carried away1. Of late, the market has been running scared from inflation pushing yields from 2% to 3%, but I think the most recent spike in the U.S. 10 year yield was as much a function of positioning as it has been about pricing in inflation. Now that the weak hands have been shaken out of the bond market, we can pause to assess.

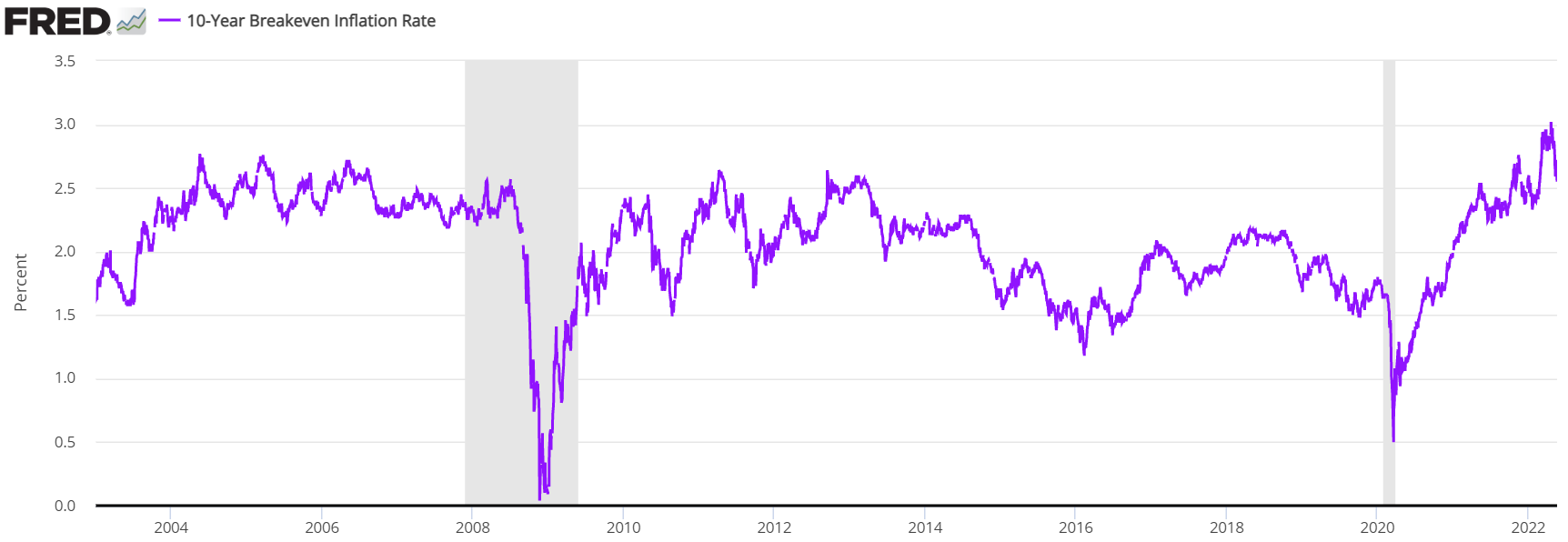

The 10-Year Breakeven Inflation Rate (that’s the difference between the nominal 10-year Treasury yield and the TIPS 10-year yield, which implies what market participants expect inflation to be in the next 10 years, on average) has jumped to between 2.5%-3.0% p.a.

I think that level of annual CPI increases is unlikely to eventuate, so I did that reverse-engineering thing I sometimes do.

Taking my (WTI YoY%)/20+2% formula that matches the CPI YoY% rate, I reverse-engineered the implied price of oil inherent in the current 10-Year Breakeven Inflation Rate. It looks like this …

Now that looks stupid! But that’s what the market is pricing in (assuming the historic correlation holds).

Nations that source their oil from Russia are switching to alternative sources, so that will result in the price of oil stabilizing or reducing somewhat rather than increase. Similarly, over the coming years the greening of the economy should begin to reduce demand … but that would increase renewables contribution to inflation, which may be more inflationary than oil - at least initially. Ultimately, the arbiter is the consumer. There are limits to what people can & will pay. If prices continue to increase, something has got to give.

The consumer is not liking the financial environment at present. There isn’t a lot of room left in their budget … especially now that debt servicing is simultaneously squeezing them from the other side.

This doesn’t bode well for the economy.

I could say more, but that’s enough for now. I’ve made my point.

Hmm, this process has been useful. I’m feeling more confident about getting into longer duration bonds [e.g. $TLT], although I wouldn’t be surprised to see one final poke back toward 3.20-3.30%-ish in the U.S. 10-year … but maybe not.

And that’s the good oil!

Continued in Part 2 …

Basically, I’m looking to time my entry to invest more heavily in sovereign bonds, and probably look to extend duration, too.