The grail quest continues

On, brave Concorde

I’ve been a bit silent of late with various holidays and, to be honest, lacking some motivation to publish anything, but there really hasn’t been anything much that has changed or required any comment.

Returning to work, what I noticed was the news and the price action are ‘one way traffic’. It can be intimidating when all the voices that are dominating the ‘conversation’ are really just the loudest voices talking over everyone. So, let’s summarize my take on conditions since my last post:

the stock market is resilient and I think it even looks like it might continue to push a little higher over the short-term

Janet Yellen has declared that an economic soft-landing has been achieved

bulls are confidently declaring positive outlooks for the market … and unable to resist ridiculing bears in the process

… but …

investor flows into stocks have been high, and that indicates to me that current price action may include more than a touch of euphoria

Source: Ned Davis Research and a certain trading model is sending a signal (see below)

My comments on the above are:

Price action is not the economy, it’s simply current sentiment.

Yellen’s comments are premature and show a blind faith in the Efficient Market Hypothesis (i.e. that all available information is ‘priced in’ by the market). However, as my research presented on this website demonstrates, that’s not how the real world works.

Sometimes I look at the market and get an idea as to how things might play out. When I returned to work and saw the euphoria, and based on my certainty that markets and the economy are going to experience ‘real world’ situations shortly, I saw a two-step scenario unfolding (see below)

Incidentally, while I’m talking about the real world, if you haven’t already, I recommend reading Howard Marks most recent post. It gives a great summary with lots of historical examples of the same things I’ve been saying on this website: leverage and the price of borrowed money shapes economic behavior … and valuations. What my paying subscribers have seen quantified is how directly that is the case from multiple perspectives.

The general theory of employment, interest and money

No, this section is not based on Keynesian economics despite the fact that I stole the title of his book for this section. I used it because it describes what I’m about to share.

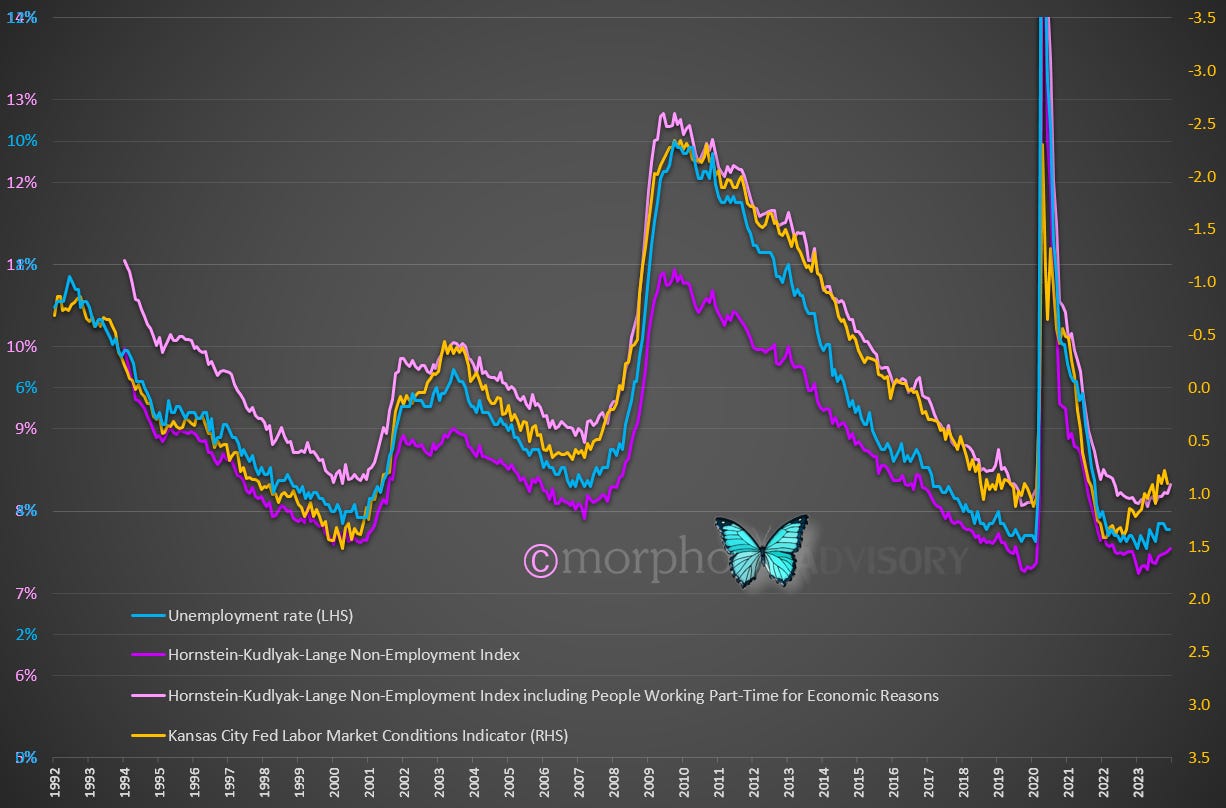

I’ve been watching employment data (as you know) and came across some new data. What I find interesting is that both data series come from Fed sources (Kansas City and Richmond). That is interesting to me because of the officialdom’s view is that labor markets are hunky dory.

Officialdom sees current low unemployment and even the slight tick back down in the last couple of months as though it was a trend. The Kansas City Fed Labor Market Conditions Indicator suggests the trend is somewhat different.

Then there’s the imaginatively named Hornstein-Kudlyak-Lange Non-Employment Index and the Hornstein-Kudlyak-Lange Non-Employment Index including People Working Part-Time for Economic Reasons.

The developers of these indices say that they are more comprehensive than the official unemployment data series. They even produced some charts that suggest that the present official unemployment rate is at risk of understating the situation, but that’s by the by because when things really start moving none of us will care to split hairs using regression models.

Here’s all these data sets shown together. I’ve had to overlay a couple of charts because I needed different scales.

All these Fed models suggest unemployment will be trending higher even if the official unemployment rate has been on a temporary hiatus in terms of its turn higher, which I suspect is related to the temporary economic uptick I talked about in Mind the Gap.

The employment situation is a function of money and interest rates charged on that money. When I looked into money and interest, I discovered some interesting things.

In order to avoid another failure of the banking system like we saw in the GFC, banks had regulation piled upon them, which made certain activities unattractive for the banking sector to take on. Banks had to apply a regulatory cost against the capital they use in their lending activities. Banks, like any business, want to make money, so they moved their focus to where the new regulations made the best economic sense.

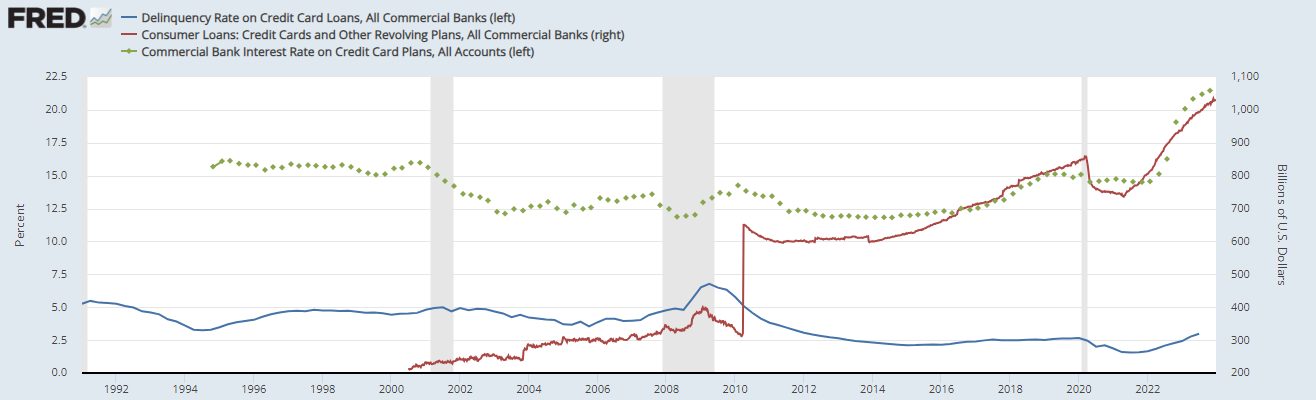

This can be seen in interest rates. Even though interest rates have risen 5%, they are still low by historic standards. But wait! There’s more.

Why then are credit card interest rates significantly higher than they have been historically? Consumers are being hit with banking regulation. Notice how the spread between credit card (unsecured lending) interest rates and other retail interest rates widened after the GFC. That widening reflects where interest rates need to be to make credit cards a viable business for banks with the high cost of capital they are required to apply.

Total credit card debt has been climbing and aligns with the change in interest rates, which suggests that many are paying minimum balances (i.e. the growth in debt is largely additional interest charges).

This does not paint a healthy picture - highest recorded level of credit card debt with the highest recorded level of credit card interest rates. It shows that there are stresses among households and consumers, which suggests delinquency and defaults will rise.

This picture is not one of a soft landing.

The trouble with our economic officials and marketing-centric sell-side financial establishment, is that they look at things in a perverse manner. Their take is like watching a sporting event, but instead of thinking in terms of the result when the athlete crosses the line or the whistle/buzzer sounds, they think in terms of who was winning for most of the time during the duration of the contest (i.e who looked better most of the time - statistically even - rather than having a results focus).