Turkey shoot

Here come the economists *gobble* *gobble* *gobble*

Regular readers may be enjoying reading recent financial news headlines and the frenzy of opinion among financial social media that accompanies data releases these days. It makes me laugh, watching the behavior of market observers because they are so surprised by the news and the changing conditions. You are observing the reactionary nature of the supposedly forward-looking financial markets.

I should’ve designed an economic Bingo card so we could all play along at home, ticking off the data and market behavior that I said was coming several months in advance as it manifested.

Earlier this month, we had July’s Nonfarm Payrolls ‘miss’ (that’s a miss relative to market expectations) plus the Sahm Rule being triggered due to higher unemployment. Denial swiftly followed and markets recovered. But denial is only the first stage of grief, next comes anger.

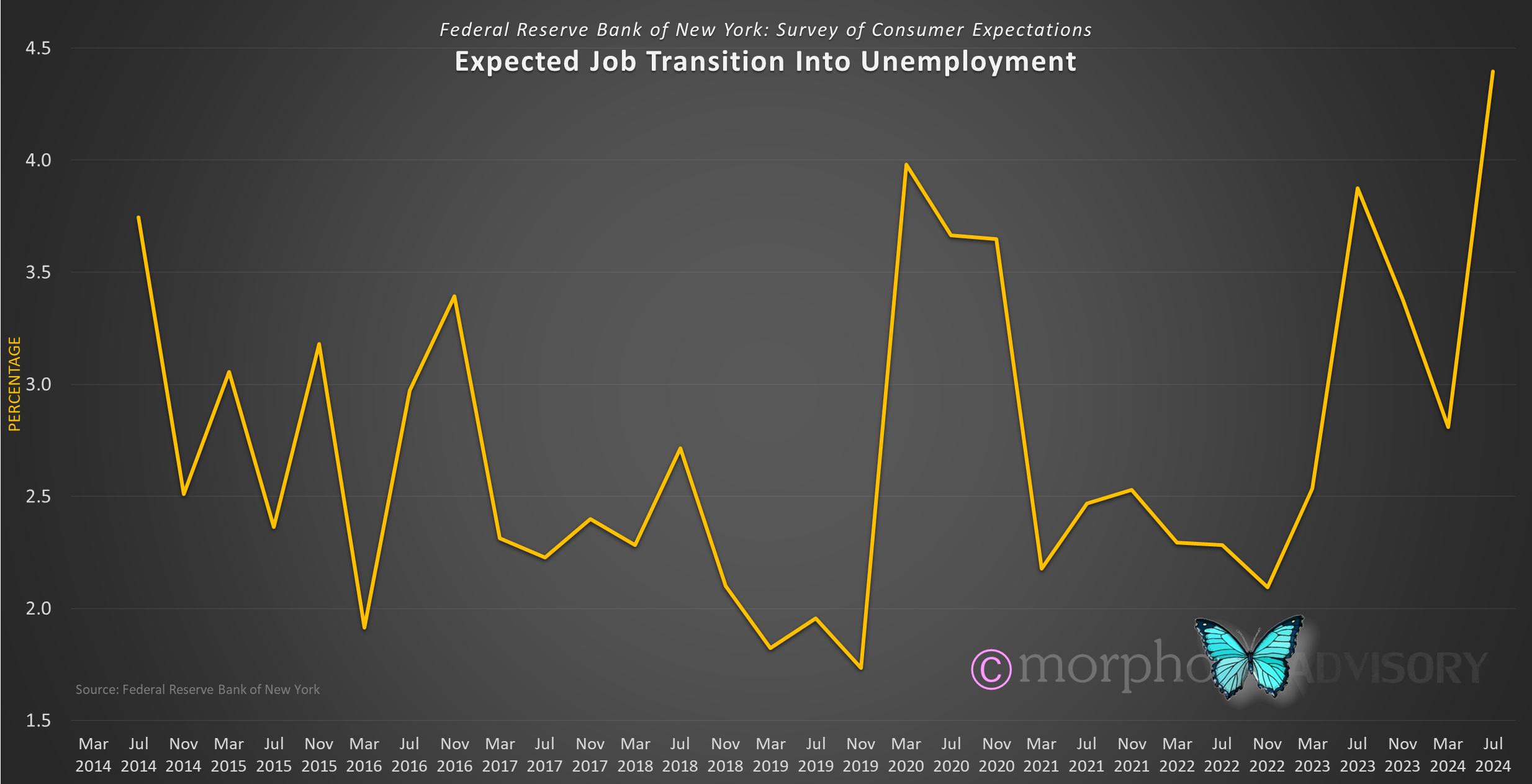

Yesterday, we had the annual revision to U.S. payrolls data, which showed 818,000 fewer jobs created in the year to March 2024. We also had the Federal Reserve Bank of New York’s Survey of Consumer Expectations report the highest level of expectation in the survey’s brief 10-year history that people will lose their job.

U.S. consumer employment expectations are worse now than they were during the height of the Covid-19 pandemic, which was a massive labor market shock that has dwarfed all historic labor market shocks. Yep, the economy is starting to turn south fairly quickly at this point.

When consumers get fearful, they hold onto their money, and when they hold onto their money the economy suffers, so people hold onto their money even more tightly.

It’s a spiral.

These consumer expectations show what is going on in the real world, not in the ivory towers of officialdom, policymakers, plus academic and Wall St economists as they consult the ancient runes of theoretical lore. That lot look down on the likes of myself because what I produce may work in practice, but it doesn’t work in theory.

U.S. consumers are also suddenly and sharply downbeat on the outlook for their income.

This is all stuff I have clearly laid out well in advance but yet, it is still coming as a surprise to the professionals. Even now, most of the professionals still think that what has proven to be historically unlikely will be the most probable outcome.

We got the last Fed meeting minutes released yesterday, too. Guess what? Looks like inflation is not the threat it once was and now there are growing concerns about the employment aspect of the Fed’s dual mandate, so a September rate cut is coming. I think I might have mentioned that in April.

Baseline

You guys know I follow this next piece of data as a key input to my economic construct.

It’s also one of those pieces of data that sneaks out there, there’s no calendar note of its impending release.

As I’ve been expecting, it’s creeping lower and has now essentially hit zero. It won’t be long before it will be negative, and that’s not good, not good at all.