A battle of wills

A cursory glance at financial social media will tell you that, in the current environment, there are strongly differing camps of opinion. In one corner we have those for whom today’s price is the sole arbiter of truth (who currently feel they are winning at life against all comers) and in the other, those who look to underlying macroeconomic data as a guide for tomorrow’s price (I am definitely in the latter group). We could further classify these two by defining the former as “traders” and the latter as “investors”, a subtle distinction.

Naturally, traders have a shorter-term horizon for their market engagement whilst investors are of the longer-term variety. I’ve said it several times before, when you get the opinion of others, you must first & foremost understand their timeframe. Social media is predominantly populated with traders who want today’s market call and whose idea of ‘long-term’ is a few days or even a week (or possibly two, but that’s stretching things a little). Meanwhile, macroeconomics mostly deals in years - a timeframe that traders can’t comprehend and so they throw out the term “perma-bear” to the likes of myself. Yes, the market nursery is as full as ever, but that’s where the learning is done … as well as the taunting.

I admit to the fact that I have been surprised by the persistence of the stock market’s continued rise, but I am unfazed and, if anything, it just makes what I plan to capitalize on all the more rewarding. Oh, yes, yes indeed it does. *rubbing hands together*

What most fail to realize is that the Covid environment has really done a number on both markets and macroeconomics alike. I said back in July of 2021 that I thought the Covid impact would have a bamboozling effect on everyone and so it continues to do.

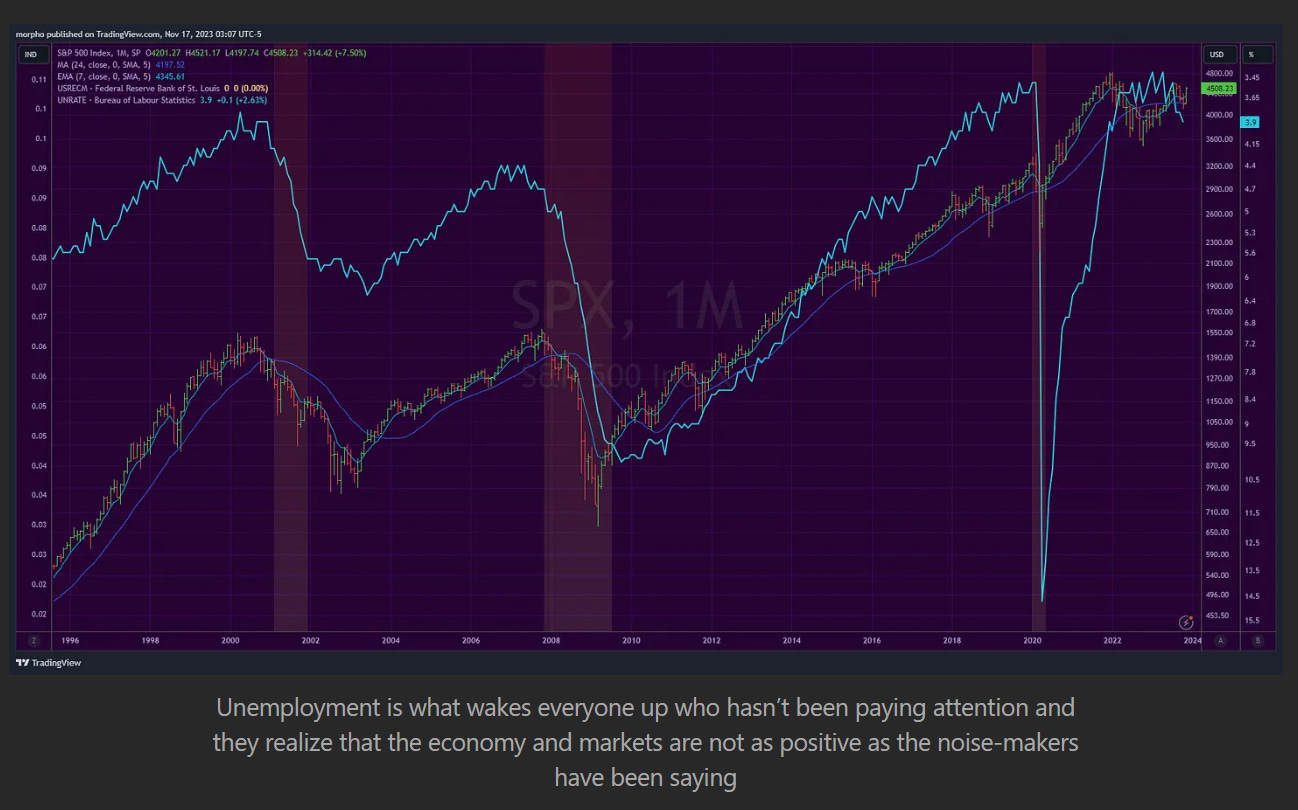

Seeing as I’m on an unemployment kick at present, let’s look at the relationship between the housing market and unemployment as an example. The massive spike in unemployment due to the exogenous shock that was Covid-19, didn’t really impact the housing market. In fact, the zero percent interest rates that Covid brought, actually re-accelerated a slowing housing market. It was only earlier this year that housing activity (Starts and Permits) dropped off … which happens to imply that unemployment will increase over the coming year (hold on to your hats as well as your jobs, folks).

The housing data in the above chart shows the macroeconomic environment - an illustration of what is going on in the underlying economy (that is to say, what is going on in the real world and not just in markets).

By contrast, what is happening in the deviant and perverse world of markets?

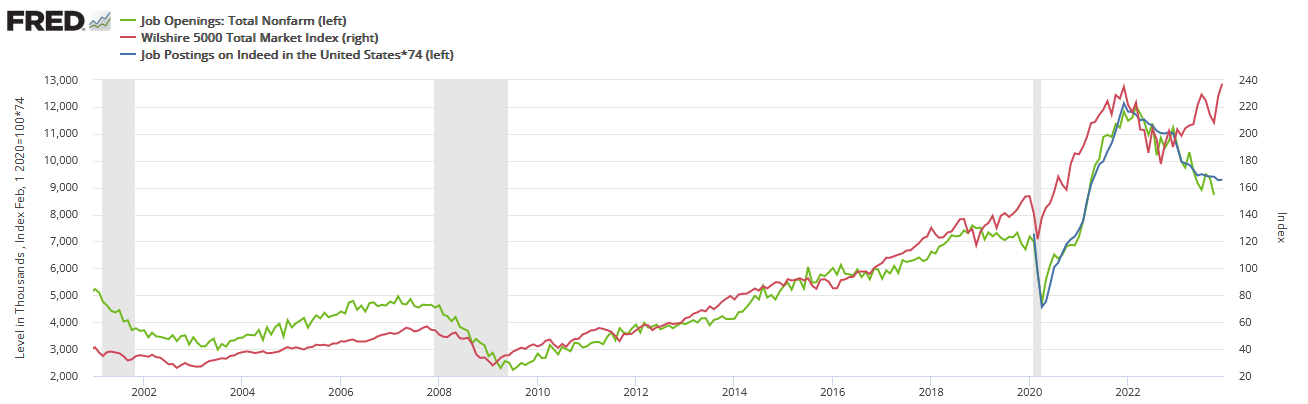

I posted the following chart a month ago …

… and have seen a very similar chart posted online recently by others but using JOLTS data instead, which shows the current divergence between macroeconomics and markets.

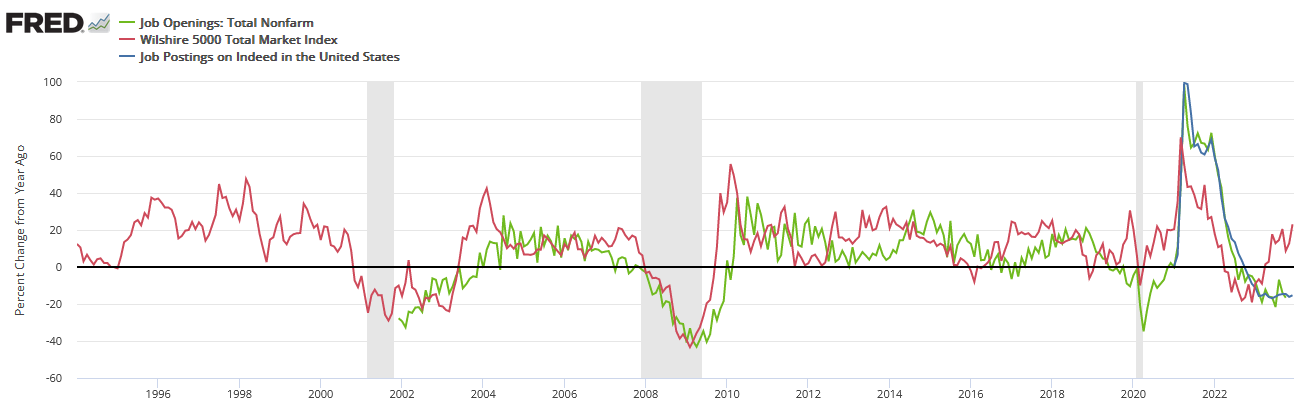

Looking at the same data on a year-over-year basis shows that while the stock market is making gains, employment markets are making losses. Curious don’t you think?

It appears the stock market is in the warm embrace of a ‘Fed pivot rally’, with the market not really understanding why the Fed should be thinking about a pivot and what it means.

Let me put it bluntly. The Fed is open to the idea of interest rates falling because there are cracking noises emanating from the economy, but those who are solely attuned to current price action aren’t on that frequency.

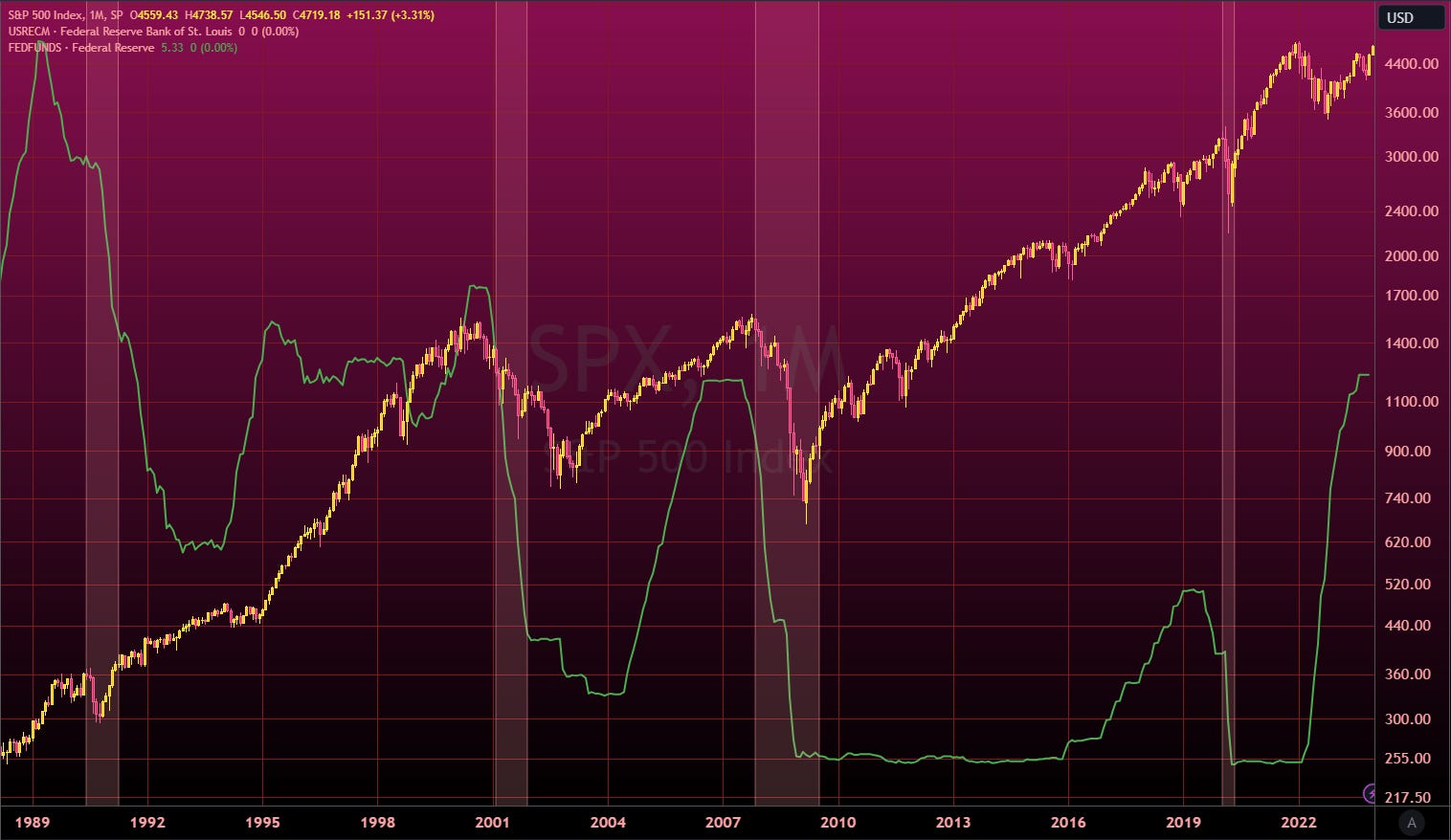

Just in case some of you are more visual, here’s a chart of the S&P 500 for the last 35 years (about the same length of time I’ve been in markets). Please note that the Fed has eased interest rates BEFORE every recession but it didn’t stop the recession (i.e. no “soft landing” except for 1995/96 and I explain the reason for this exception here and here and why the current cycle doesn’t fit with ‘exception’ criteria), nor did it stop the market from experiencing a significant drawdown.

Short-termism

A case in point regarding how misleading the short-termism of traders can be, I don’t know if you’ll recall, it was so long ago in market terms, but all the world was hating on bonds approximately 3-months ago. Financial social media and others were hating on bonds as yields rose, and one major clown prominent ‘personality’ from the hedge fund world said ‘I don’t like bonds’, which is when I said ‘I like bonds’ not once, but twice. In that first post, I said that we were near a “turning point of some significance”. Funnily enough, bonds delivered their best returns in 40 years in the month of November.

On top of November’s bond rally, this week’s Fed pre-pivot pivot (soft pivot?) news has delivered another kicker benefiting bond returns this month, too.

I point this out to illustrate two things:

short-termism (including bandwagon behaviors) and social media idiocy should be tuned out;

when the market finally aligns with turns in the macroeconomic cycle, things can happen swiftly and bigly.

I guess I’m saying that macroeconomic-guided investing is similar to a soft-form style martial art like Tai Chi rather than a day-trader’s hard form, akin to Karate. I prefer my gong-fu to use the energy of others (many others) for my substantial gain rather than to exert undue amounts of my own energy in a combative style for small gains.

I use the willfulness of others, moving backward and ignoring their taunts, feeling their energy as they expend it, all the while laughing at my foolish ways. But the data doesn’t align with their lips, like a poorly dubbed movie.

May your investing chi flow effortlessly.