Delinquent Tendencies

Follow the money

Once in my youth I was associated with a group of people that you could describe as having delinquent tendencies, which was a bemusing experience for me. It was in college (what our American friends call “High School”) and I was put on ‘Log Book’. This required me to get my teachers to sign the log book after every class. In a school of some 800 students, I was one of a handful of people who had to go through this trying experience. All of the others on Log Book had delinquent tendencies. These were young men who had no interest in school and would leave as soon as they were permitted by law, were always getting into trouble with authority, and for whom rules had an optional existence. They weren’t unintelligent people, but they were not academically oriented. By putting me on a strict reporting regime alongside this group of people, I was made to feel stupid and a problem child by association, neither of which come close to describing me. In hindsight, it was mostly likely due to me being on the autism spectrum. In reality, the education system stole the joy of learning from me (someone who used to read encyclopedias as a child) and I put in minimal effort, plus the abstract-based academic teaching methods were befuddling and, quite frankly, inferior to my own method of learning. Anyhow, I left the education system feeling barely adequate as a human being despite having passed my exams.

To my mind, our education systems are as much about unconscious social conditioning as they are about education: ‘We will set the standards of “success” to which you must aspire. You must fit in!’

The only other delinquent activity I participated in was Entering. I differentiate it from Breaking & Entering because I didn’t break anything, just entered these large, empty-for-the-weekend establishments. My friend(s) and I were into running and sometimes on our weekend escapades we would enter these properties and just run around. It was adventurous rather than criminal. Youthful mischief.

But enough of this wandering down memory lane. That’s not the sort of delinquency I am wanting to discuss.

There’s trouble at t’mill

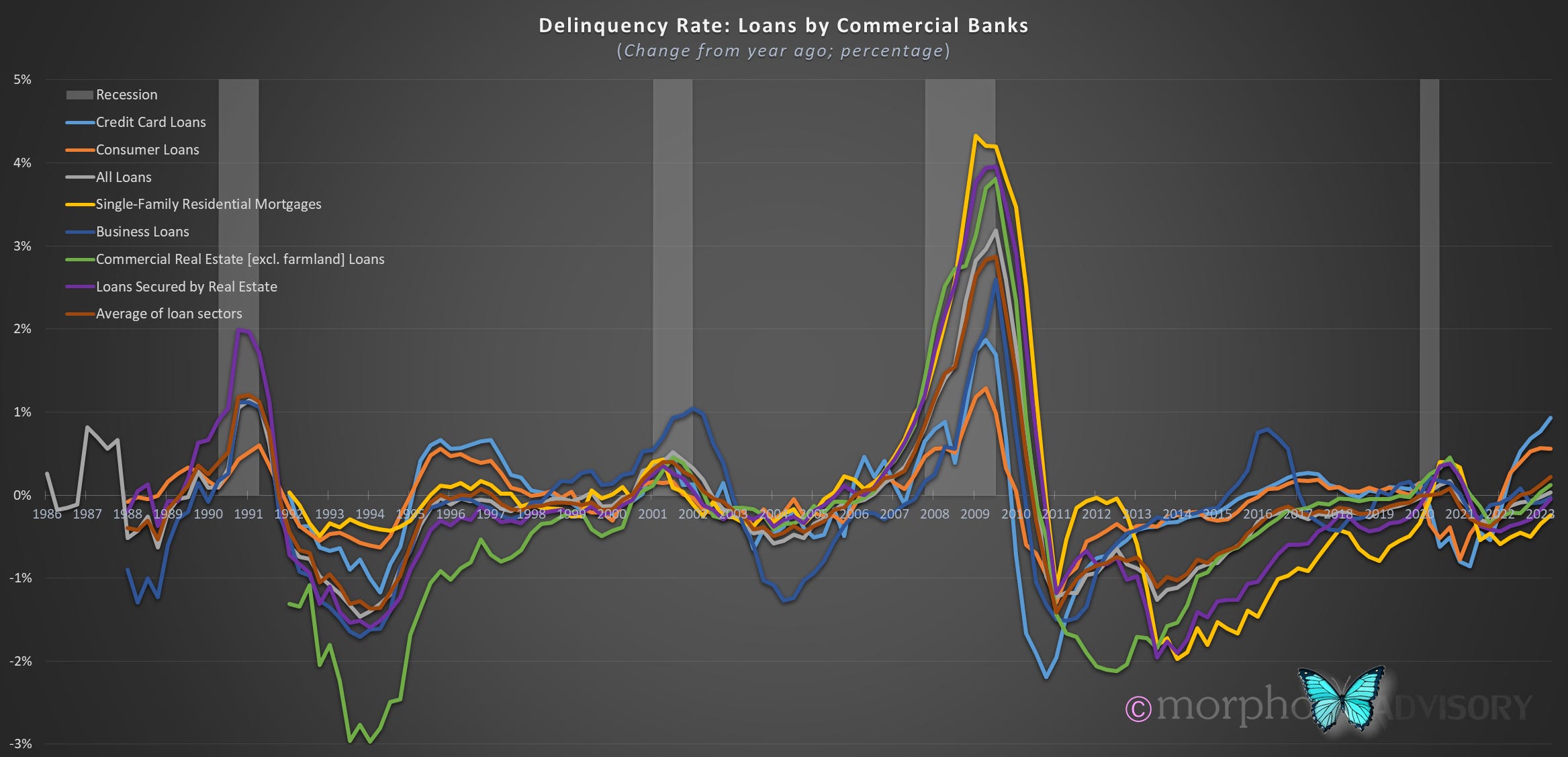

Reading back through my posts, you’ll know that I’ve called for economic recession some time back and that it’s gone from ‘probably in 2023’ when I first mentioned it in 2021 to now that 2023 is here, being ‘the data says we’re in it now, but it won’t be confirmed “officially” until 2024’.

My slowly returning curiosity (after being bed-ridden for the last couple of weeks) led me to investigate loan delinquency data. I dug up a bunch of data series of different types of loans and frew dem at a chart whuch got me finking many fings (i.e. my curiosity exploded with thoughts and ideas of what the various data series might suggest goes on throughout macroeconomic cycles in the realm of human behavior).

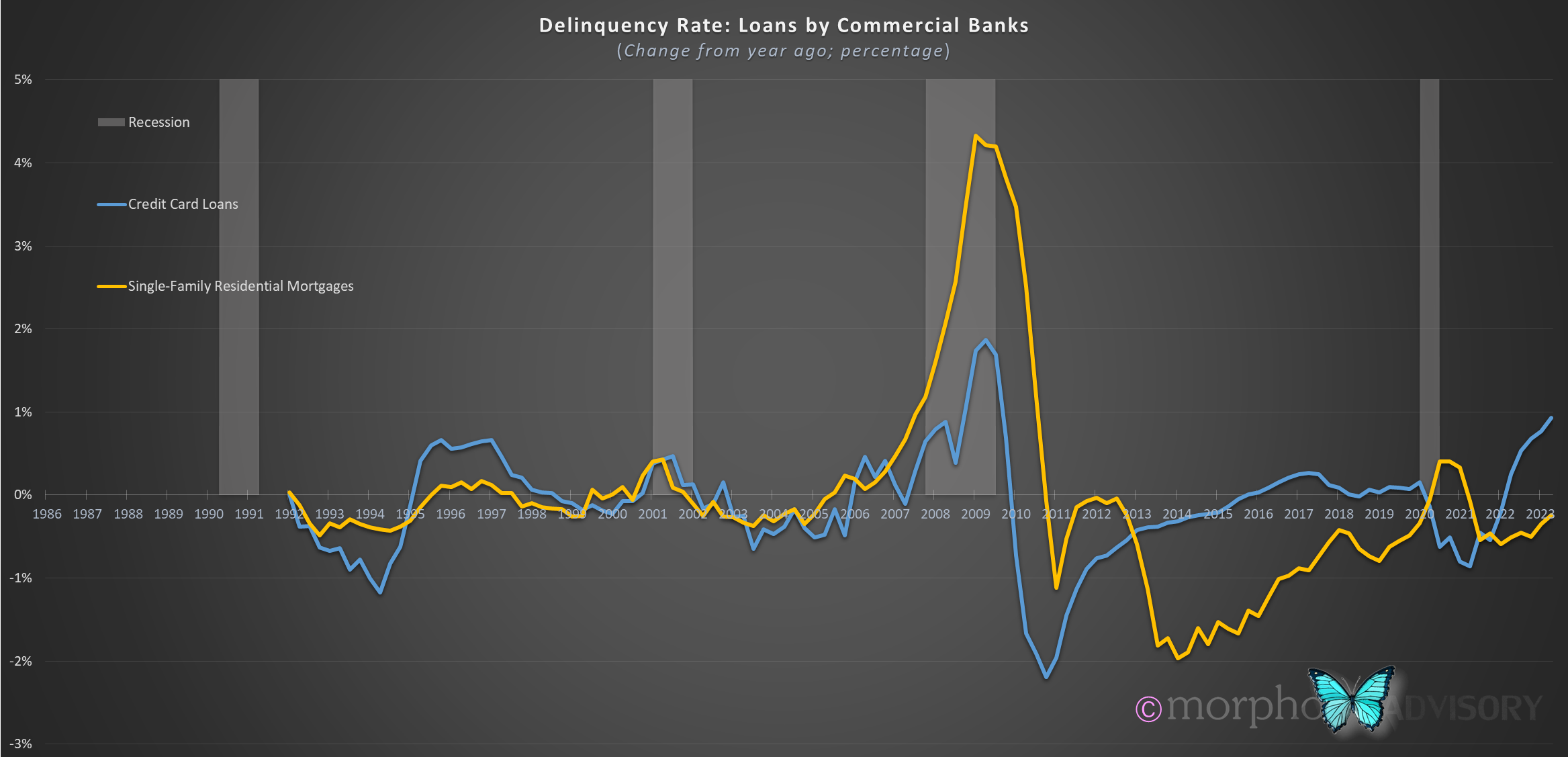

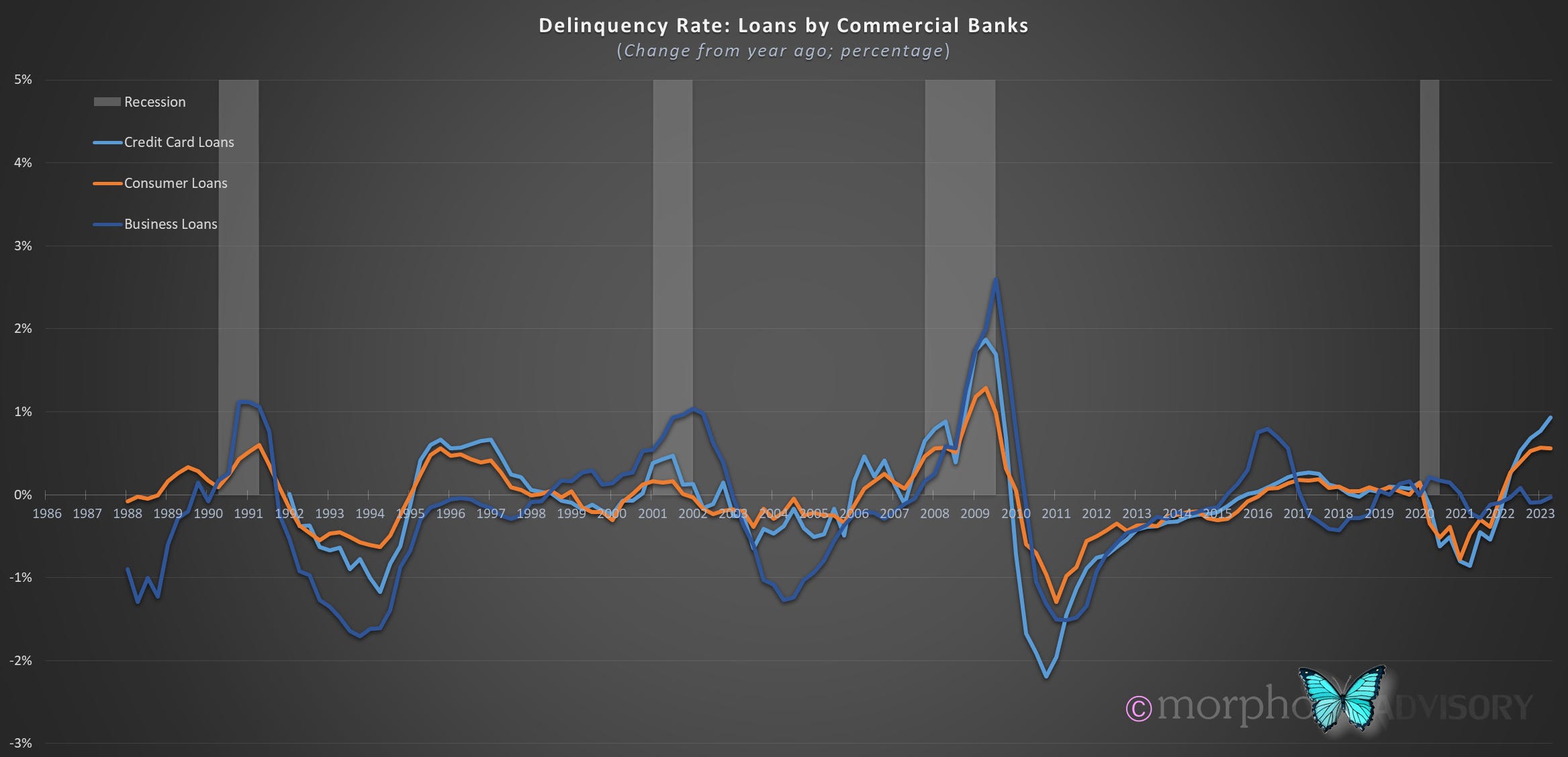

Hmm, apart from the obvious increasing loan delinquency at the current point in time and the upward trend in those loan types that are not yet showing increased delinquency, what was the first thing that hit me? That mid-1990’s “soft landing” period, which I attribute to the Millennial generation entering the economy and so offsetting the rising interest rates. Even though consumer loans were impacted, as were single-family real estate, loans to the rest of the real estate sector and businesses were doing OK. It was too soon for the Millennials to be tied into property ownership and be constrained by a rate hike cycle (i.e. have high fixed cost structures as a cornerstone of their life … apart from student loans), so they added support to businesses and commercial real estate sectors whose loans didn’t move into delinquency. Seeing this in data form spread across various sectors gives me more confidence in my thesis that it was demographics that resulted in the “soft landing”. It also makes me think that consumer loans (including credit cards) are closely associated to property ownership and are used as a form of liquidity by homeowners who are living up to the limit of their means.

The problem in the current environment is that property owners are now stuck in their homes. Liquidity is drying up. They can’t sell because that would expose them to refinancing and move their interest rate from around 3% to 8%. Ouch!

People can't refinance (or consolidate their debts) without resetting their mortgage rate, so they have to use credit cards or personal loans for liquidity. Tightening credit conditions in addition to higher interest rates is resulting in increased personal loan & credit card delinquency. What is occurring in the economy is a cash flow and credit squeeze. Even if the Fed did pivot to pause (i.e. no longer having a tightening bias) just holding rates at current levels prolongs the financial pressure on households. It is like putting a physical structure under pressure beyond its engineered tolerances. Eventually, it will have to give and ruin awaits some, but not all.

It is always those at the margin that will suffer the most. I’ve pointed out before that only 4% of residential real estate trades every year, but it is those marginal transaction valuations (e.g. being ‘stopped out’ via foreclosure etc.) that impacts the wealth (i.e. the perceived value of their assets) for all … and the banking sector’s willingness to lend up to certain levels. So, while most will not face financial ruin, everyone will feel poorer, and that impacts spending habits, and where the consumer goes, so too does business.

And when business suffers, they start cutting costs.

Action, reaction

As I was pondering all this delinquency data and the various human behavioral aspects it implied, I looked at changes in valuations of two major asset class over the last few decades.

I found it interesting that there was an alternating pattern between the two.

The stock market dip in 1990 was both short and small, but it was the first time that slower moving (and leveraged) property values had dropped for decades. The following decade was when stock values took off and went to extreme levels of speculation. Then the Dot-com crash wiped that out while property values remained up, so the next cycle everyone speculated in real estate. Then that got wiped out ….

This time, there is no place to hide in either of these two sectors. Equities are priced beyond any form of rational expectation, and real estate is facing a long, slow headwind. The major property owning demographic are the Baby Boomers who are approximately 70 years old on average. Worse still, the U.S. life expectancy is lower than most developed nations, being just under 80 years on average. Only 10 years until there will be an oversupply of property, a-la Japan and Italy. Caveat emptor.

What are the likely knock-on impacts?

We have priced our children out of the property market. I’m not even sure it’s an aspiration of theirs (they want to travel), which many older people can even conceive.

They are therefore not bound to a geographic location and technology further enables this.

They are also not engaged in family formation (i.e. making babies … which is the engine of tomorrow’s economy).

Local government is funded by property taxes. Not only does this compound the cost of property ownership for the younger generation getting “on the property ladder” - which in their case will be a descending ladder - (in addition to having to finance the oldies retirement via government taxation), but it means local government and their infrastructure financing activities will become less viable.

Nations will begin competing for immigration (i.e. people to fill jobs … and a source of tax revenues). It’s likely that incentivized tax residency will be offered (even if not physical residency) just like corporates get.

It has already begun. Canada has a big immigration drive. Here in NZ, Australia is advertising for NZ Police officers to move over there. NZ is talking of doing it to source teachers.

It’s a brave new world we are entering, one that has a vastly different value system to the one we have known for the last 70 years. We must all take the unofficial slogan of the U.S. Marines to heart:

Improvise, Adapt, and Overcome

Hold a light attachment to beliefs and things, and be willing to release, let go and change. Stay light, nimble. Better still, refine your core values to their underlying essence and hold only to those. All else can, and will, change.

Even elderly people in Japan eventually resorted to committing petty crimes in a virtually crime-free society so that they could be caught, imprisoned and thus have food, shelter and medical care provided.

I don’t want my kids burdened by bureaucratic structures that have been built presuming that past results guarantee future performance when in reality we’re actually delivering them a ‘hospital pass’ that is essentially a ponzi scheme.

Anyhow, dwell on that lot and if need be make plans.

As I often remind people, economics is extremely slow moving. My view has not changed for 2 years and so far I have been correct on the big picture. It’s unfolding just as I have said (the details have been volatile, but the main stuff is accurate). By contrast, the financial media and our financial authorities have vacillated in their outlook being confused about how this shit show works.

PS. that 68% fall in the U.S. stock market is still on.