Exegetical bullseye

Some time back, I looked at delinquency data and made an observation, based on how the delinquency statistics on different loan classes behaved at a particular point in time (the mid-1990’s) and based upon my view that demographics caused the mid-90’s “soft landing”, that consumer loans and credit card debt are closely tied to home ownership.

Two bits of information have come to hand more recently that validate my interpretation.

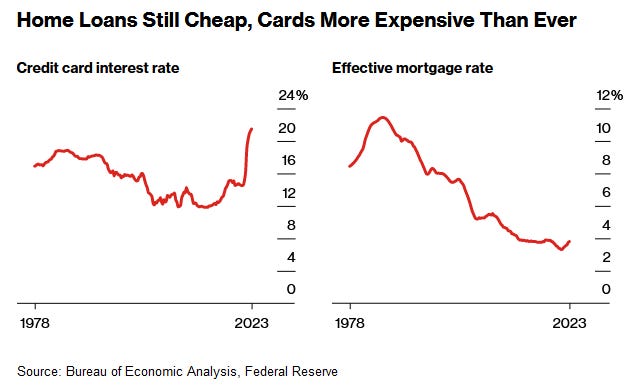

Firstly, a couple of weeks ago, I was told by a U.S.-based hedge fund manager that the U.S. mortgage market is peculiar in that borrowers primarily take on a 30-year fixed rate mortgage, but when interest rates fall, they simply refinance. In this way, they are protected to the upside, but can capture the downward move in interest rates. This explains why the average interest rate on U.S. home loans remains in the vicinity of 3% (close to the all-time-low) despite the current interest rate being around 7% (close to the long-term average for the last 30-years).

The flipside to this ‘free option’ that U.S. borrowers have - and which they have been discovering lately - is that, all that easy credit has them cornered when interest rates turn upward in a sustained manner. They can’t refinance their homes to access capital (e.g. for purchases, repairs or bill payments etc.) because that would make their borrowing cost more than double. Trapped! This is why existing home sales and inventory have fallen while new builds have grown. Any movement on existing property will expose borrowers to current interest rates. So, the credit card is the homeowner’s ‘go to’ in times like these, an easy line of credit to keep themselves liquid.

Crunch!

Remember how a little while back I pointed out that credit card interest rates were at all time highs even after 40 years of falling interest rates? This is due to how post-GFC banking regulation penalized unsecured lending, so that line of business needs to be more profitable if banks are to be enticed into deploying their risk-weighted capital in that direction.

It turns out that new regulation to fix one problem (e.g. banking post-GFC) creates a new problem elsewhere through risk transfer (e.g. U.S. household liquidity/illiquidity during a rising interest rate cycle).

How bad is the situation?

That brings me to the second lot of information that has come to hand. This last week, Bloomberg essentially summarized the two articles I wrote previously (links above), but with the added bonus of some nice charts.

When you’re strapped for cash, it’s cheaper to pay 20% interest on a few thousand dollars than double your borrowing cost on a few hundred thousand dollars.

The problem is, the longer that interest rates remain elevated, that 20% interest rate compounds and things accelerate quickly. This is why we saw prudent borrowing behaviors in the 1980’s when interest rates were last near these levels, but current conditions all happened so fast that consumers didn’t have the two prior decades of rising interest rates to acclimatize themselves to a higher rate environment like folk in the ‘80’s did.

U.S. households now pay as much interest on other forms of borrowing as they do on their mortgage repayments.

Now you may get a sense of how large and how fast the rate rises from March 2022 to July 2023 are in historical terms, and why the notion of a “soft landing” is and always was, ignorance gone to seed.

However, even the Bloomberg article from which these charts came ended by saying that things weren’t a problem because debt servicing as a percentage of U.S. household income is low by historic standards.

But I think Bloomberg’s conclusion is wrong. And do you know why?

You guessed it. We have an increasing number of households that don’t have any debt and are earning an income. Retired people living on a pension. Boomers!

What if we adjust the chart immediately above by Older Dependents to Working-Age Population and see if that alters the picture because, intuitively, the chart above doesn’t make sense - it should be higher. Yes, interest rates are historically low (locked in around 3%), but there is significantly more debt in the system than anytime over the last several decades AND developed nation households always live up to the limit of their means - that’s why asset prices get pushed higher and higher as interest rates fall.

If working-age population households are cash strapped, as interest payments on non-mortgage debt suggests they are, where will all the growth in consumer spending come from? Maybe from retired people who can earn more in interest income. Oh, that’s right. U.S. households have the majority of their retirement savings in equities. That’s a tenuous position when we have a slowing manufacturing sector that confirms consumers are having their disposable income eaten by inflation and interest rates, and why businesses are now looking at cost-cutting (aka lay-offs).